When MSCI Emerging Markets Becomes One Trade

Where year-to-date emerging markets index returns are actually coming from — and how the RAM Emerging Markets Equities strategy is positioned relative to it.

Summary

The MSCI Emerging Markets Index has returned +25.61% year-to-date in 2026 (Net Total Return, USD, through 2026-05-29). Behind that headline, the contribution distribution is extremely narrow. On the sector dimension, Information Technology alone contributed +25.19 percentage points — more than the entire price-based aggregate of the index. On the country dimension, South Korea contributed +15.49pp and Taiwan +12.30pp, together accounting for +27.79pp. Every other sector and country in aggregate has been close to flat or detractive.

The implication for investors: a passive allocation to the MSCI EM Index in 2026 has not been a diversified exposure to the asset class but a concentrated exposure to a single global theme, expressed through the same handful of names whether read along the sector axis or the country axis. The two axes are not independent; they reinforce one another, because the largest sector exposure (Information Technology) lives almost entirely in the two largest country exposures (Taiwan and South Korea).

The RAM Emerging Markets Equities strategy is constructed with the aim of offering access to various Emerging Markets themes and reducing concentrated bias present in the index. Across the eight largest AI hardware names in the MSCI EM Index, the strategy carries 18.5% of fund NAV against 33.1% in the index — an active underweight of 14.63%. The two charts on the next pages decompose the index's year-to-date return on each axis. The following pages document the strategy's positioning and historical risk-return profile.

This document is descriptive and informational. It does not constitute investment advice, an investment recommendation, a solicitation, or a forecast of future returns. All figures are computed from MSCI/FactSet benchmark composition data, RAM AI internal position records, and Bloomberg price series. Past performance is not a reliable indicator of future returns.

Concentration and the Strategy's Active Position

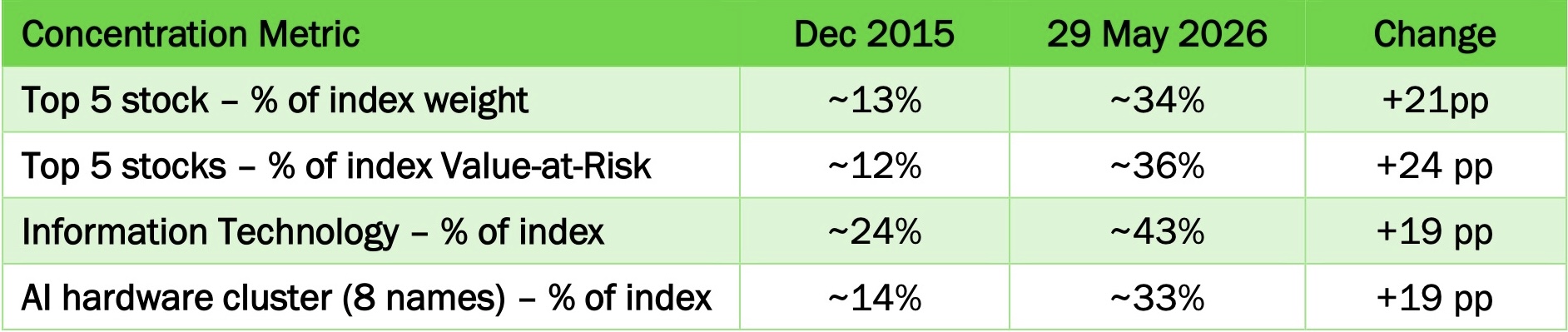

The structural concentration of the MSCI EM Index has roughly doubled in a decade. The top five names account for approximately 34% of the index by weight today, against approximately 13% in December 2015; their share of the index Value-at-Risk has tripled over the same period, from approximately 12% to 36%. The strategy's underweight of the eight-name AI hardware cluster is concentrated in the largest three constituents.

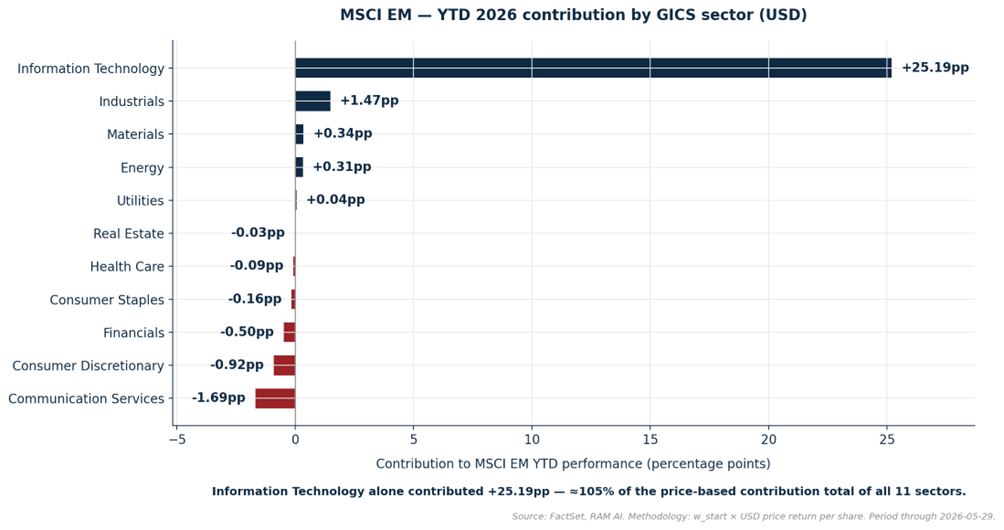

YTD 2026 Contribution — By GICS Sector

Information Technology contributed 25.19 percentage points to the index’s year-to-date return, driven by semiconductors and memory. The remaining ten GICS sectors, taken together, contributed close to zero. Three sectors detracted materially: Communication Services, Consumer Discretionary, and Financials. On the price-based decomposition (which excludes dividend income), Information Technology's contribution of 25.19pp alone exceeds the 23.94pp aggregate of the entire index.

The chart shows that the entire year-to-date return of the MSCI Emerging Markets Index has been delivered by a single sector. This is not a one-month effect; it is the result of five months of cumulative price action concentrated in semiconductors, memory, and AI-server hardware. The RAM Emerging Markets Equities strategy is underweight Information Technology by 15.84 percentage points (27.35% of fund NAV against 43.19% of the index), the largest single sector active weight in the portfolio by absolute magnitude.

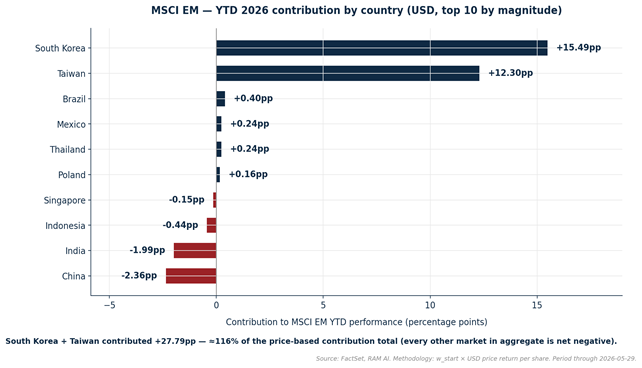

Same Story Read by Country

Two countries deliver year-to-date contribution that exceeds the index's aggregate return. South Korea contributed 15.49pp from a starting weight of 13.21%, implying an aggregate country return in the order of 117% in USD, led by Samsung Electronics and SK Hynix. Taiwan contributed 12.30pp from a starting weight of 20.52%, implying an aggregate country return in the order of 60% in USD, led by Taiwan Semiconductor. China and India — together 40.03% of the index by starting weight — detracted 4.35 percentage points in aggregate.

Source: FactSet. Data from 31st December 2025 to 29th May 2026.

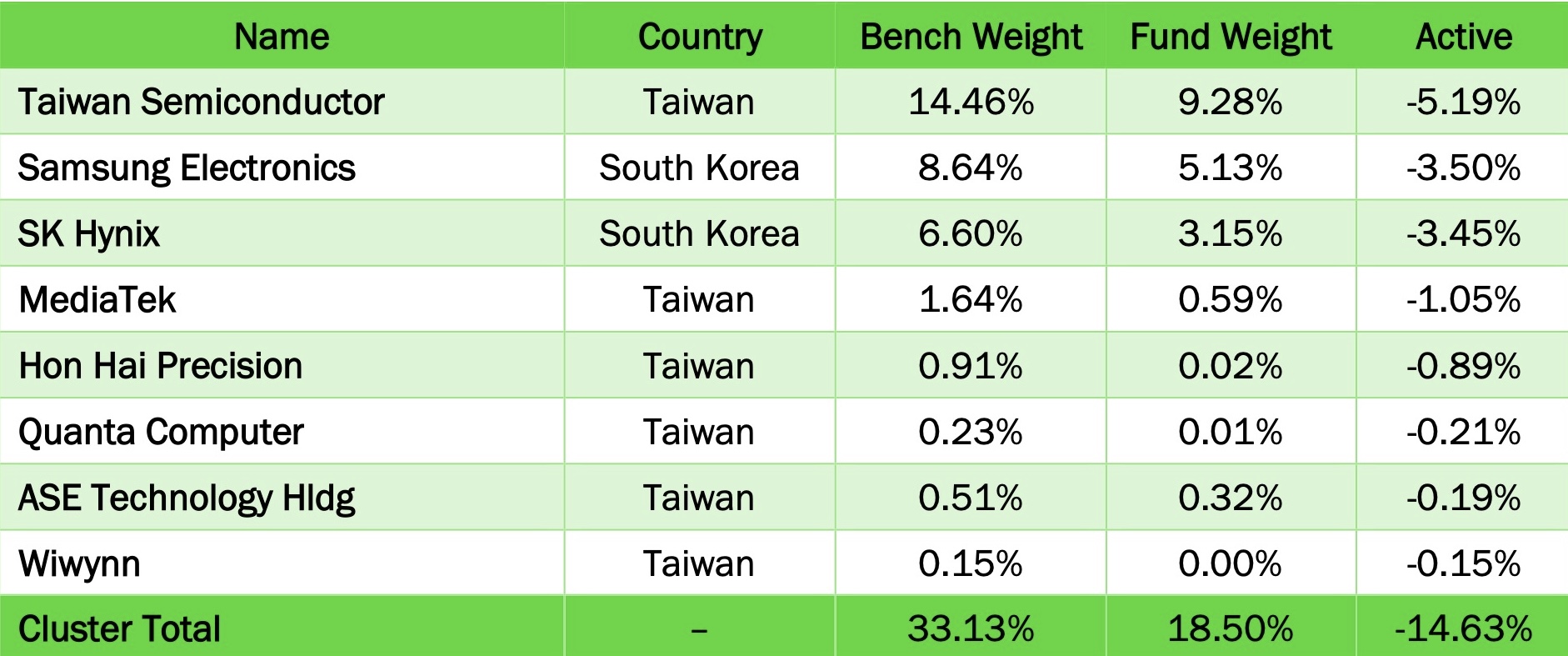

The sector and country decompositions describe the same underlying concentration. The largest individual stocks — Taiwan Semiconductor, Samsung Electronics, SK Hynix — sit in the index's largest sector and its two largest country exposures simultaneously. The strategy's active position on these names, detailed in the table below, is the dominant driver of its year-to-date relative performance on both dimensions.

Active Positions on the AI Supply-Chain Cluster

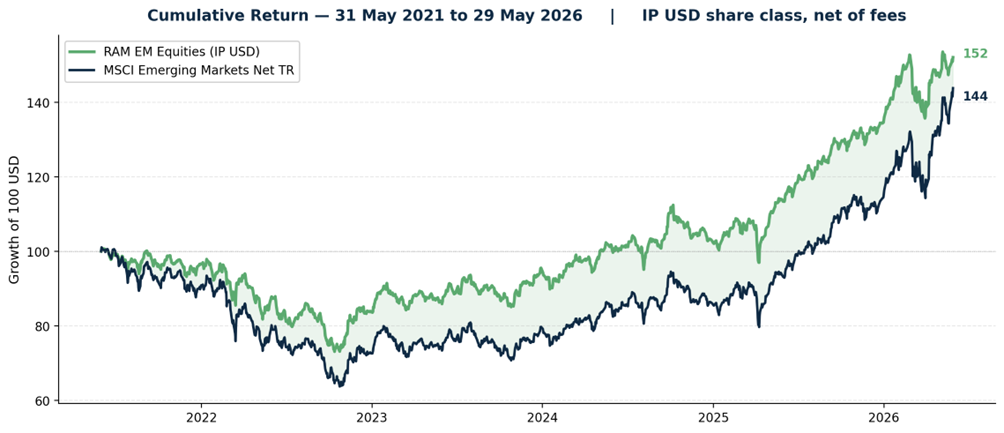

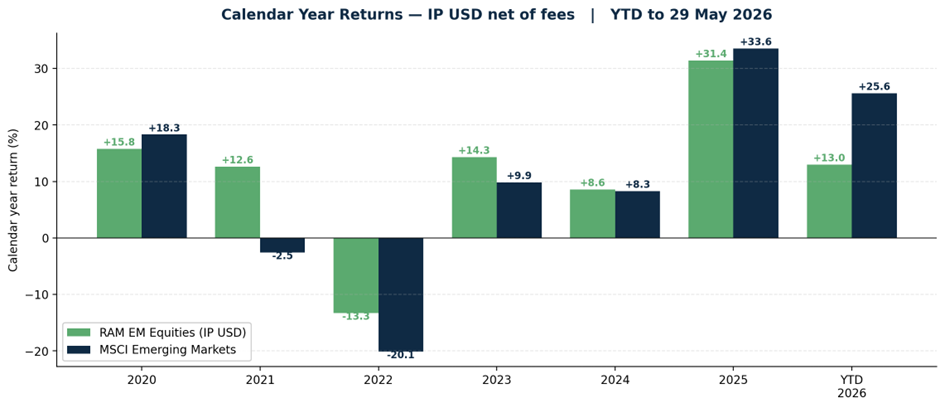

RAM Emerging Markets Equities Strategy’s Five-Year Cumulative Performance

Conclusion

The MSCI Emerging Markets Index in 2026 has concentrated its year-to-date return delivery on a narrow set of exposures. Information Technology contributed 25.19 percentage points to the index's year-to-date return; on the country dimension, Taiwan and South Korea together contributed 27.79 percentage points. The two readings describe the same underlying position: the three largest individual constituents (Taiwan Semiconductor, Samsung Electronics, SK Hynix) sit at the intersection of the index's largest sector and its two largest country exposures.

The RAM Emerging Markets Equities strategy is positioned against this concentration on each axis. At the cluster level, the active underweight stands at −14.63% (18.5% of fund NAV against 33.1% in the index across eight AI hardware names). At the country level, the strategy is underweight Taiwan by 8 percentage points and South Korea by 11 percentage points. At the sector level, the underweight to Information Technology is 16 percentage points. The offsetting overweights are distributed across Consumer Staples, Consumer Discretionary, Health Care, Energy, and across countries that the cap-weighted benchmark structurally under-represents.

Over the multi-year windows documented above, this construction has produced a positive annualised excess return at lower realised volatility than the index, with an asymmetric monthly capture profile that compresses in narrow leadership regimes. The figures presented in this note describe the resulting composition and the realised risk-return profile of the strategy. They do not constitute a forecast or a recommendation.

Image Gallery

Legal Disclaimer

Glossary

Alpha

Alpha is used in finance as a measure of performance. Alpha specifies the difference between the performance of the sub-fund and the theoretical performance of the market it is exposed to, indicated by the beta. Alpha is generally used to measure the added value of the portfolio manager. A positive alpha indicates that the sub-fund has performed better than the performance linked to its beta. The excess return of an investment relative to the return of the respective market exposure is the investment's alpha.

Beta

Beta represents a sensitivity of a sub-fund against market movements, it is used to evaluate systemic risk. Beta is a measure, through time, of the linear link between performances of the sub-fund and a benchmark. The beta is obtained by calculating the regression line of performance of the sub-fund above the risk free rate and the performance of the benchmark. A beta above 1 indicates that the sub-fund tends to amplify market movements whereas a beta below 1 tends to nuance such market movements, suggesting a more defensive approach.

Delta / Equity Sensitivity

The ratio comparing the change in the price of the underlying asset to the corresponding change in the price of a derivative.

Duration

The duration represents the length of time for which capital is "tied-up" in a bond investment. In contrast to residual maturity calculations, the concept of duration takes account of the time structure of returning cash flows (such as coupon repayments). The average duration of the portfolio is derived from the weighted average duration of the individual securities.

Max Drawdown

The Max Drawdown is a measure of extreme downward risk, corresponding to sub-fund performance calculated at the worst possible timing, i.e. between the highest and the lowest point of its value, neglecting price movements in-between. This measure represents the estimated possible maximum loss an investor could face on the given period.

Modified Duration

The "modified duration" is derived from the duration and provides a measure of the risk with which the sensitivity of bonds or bond portfolios to interest-rate changes can be estimated. A 1% increase (decrease) in the interest level accordingly produces a percentage fall (rise) in the price in proportion to the modified duration. For example: the modified duration of a bond fund is 4.5, the theoretical yield to maturity is 5.3%. If the yield drops by 1% to 4.3%, the fund price increases by around 4.5%.

Rating

The credit Rating is a parameter used by banks and lending institutions to determine whether an applicant is deserving of the confidence necessary for the granting of a loan. This parameter makes it possible to measure the risk of consumer default and determine the economic conditions applicable to consumers. The highest rating is indicated by the letters: AAA. This is the indication of highest financial security. This is followed by: AA, A, BBB, BB, etc. The lowest credit rating corresponds to the letter C. This letter identifies a high risk of financial default and is a figure taken into great consideration by each lending institution.

Sharpe Ratio

The Sharpe Ratio is a risk-adjusted performance measure, calculated as the performance of the sub-fund above the risk-free rate divided by the standard deviation of the performance. The higher the ratio the better the sub-fund has performed, as the sub-funds marginal outperformance is higher per unit of risk. A negative Sharpe ratio indicates that the sub-fund has not outperformed the risk-free return.

SRRI (Synthetic Risk & Reward Indicator)

The SRRI represents the risk and return profile as presented in the Key investor document (KID).

Volatility

Amplitude of the variation of the price/of the value of a security, a sub-fund, a market or an index, measuring the importance of risk over a given period. Volatility is calculated through the standard deviation obtained through calculating the square root of the variance. Variance being the average of the squared differences of deviations from the mean. The higher the volatility, the riskier the security, the sub-fund may be.

Yield-to-maturity

Weighted average annual rate earned by an investor who buys the bond portfolio today at the market price and holds the bond portfolio until maturity, and assuming that all coupon and principal payments will be made on schedule.

Yield-to-Worst (YTW)

Weighted average potential annual rate that can be received on a bond portfolio without the bond issuers actually defaulting. The yield to worst is estimated by making a worst-case scenario assumptions on the issue by calculating the returns that would be received if provisions, including prepayment, are used by the bond issuer. Yield to worst may be the same as yield to maturity but never higher.

Performance Fees

Performance is charged on any returns that, subject to High Water Mark, the sub-fund achieves above its performance fee hurdle rate (if any). Please refer to the Prospectus for further information

Ongoing charges

Ongoing charges are based over 12 months of expenses ending the 31 December of the previous year. It is annually updated, but may be adjusted more frequently. Performance fees and portfolio transaction costs are excluded except in the case of an entry/exit charge paid by the sub-funds when buying or selling units/shares in another collective investment undertaking. Estimate of future charges is used for funds younger than 12 months.

Disclaimer

Important Information:

This document is provided for information purposes only to professional clients and is descriptive in nature. It does not constitute, and shall not be construed as, an offer to buy or sell any financial instrument, an investment recommendation, investment advice, a solicitation, or a forecast of future returns. The fund referenced is a Sub-Fund of RAM (Lux) Systematic Funds (Luxembourg SICAV, CSSF, UCITS Directive 2009/65/EC); not offered for sale in the United States or to any US Person. Past performance is not a guide to current or future results. Forward-looking statements reflect the views of the Systematic Equities team as of the publication date, are subject to change without notice, and are not guarantees of future performance. Issued in Switzerland by RAM Active Investments S.A. (FINMA); in the EU/EEA by Mediobanca Management Company SA, 2 Boulevard de la Foire, L-1528 Luxembourg. Please refer to the KIID and prospectus before considering any investment.

The sub-fund mentioned above is a Sub-Fund of RAM (Lux) Systematic Funds, a Luxembourg SICAV with registered office: 14, Boulevard Royal L-2449 Luxembourg, approved by the CSSF and constituting a UCITS (Directive 2009/65/EC). Mediobanca Management Company S.A. 2 Boulevard de la Foire 1528, Luxembourg, Grand Duchy of Luxembourg is the Management Company.

Please note that the share classes mentioned in this document may not be registered in your country of domicile.

This marketing document is only provided for information purposes to professional clients, and it does not constitute an offer, investment advice or a solicitation to subscribe shares in any jurisdiction where such an offer or solicitation would not be authorised or it would be unlawful. In particular, the Funds are not offered for sale in the United States or its territories and possessions, nor to any US Person (citizens or residents of the United States of America).

This document is confidential and is intended only for the use of the person to whom it was delivered; it may not be reproduced or distributed.

There is no guarantee that the holdings shown will be held in the future. The investment described concerns the acquisition of shares in the Sub-Fund and not in a specific underlying asset.

Past performance is not a guide to current or future results. There is no guarantee to get back the full amount invested. The performance data do not take into account fees and expenses charged on subscription and redemption of shares nor any taxes that may be levied. As a subscription fee calculation example, if an investor invests EUR 1000 in a fund with a subscription fee of 5%, the investor will pay to his financial intermediary EUR 50.00 on the investment amount, resulting with a subscribed amount of EUR 950.00 in fund shares. In addition, potential account keeping costs (by investor’s custodian) may reduce the performance. Some shares in the Sub-Fund apply a performance fee. Leverage intensifies the risk of potential increased losses or returns.

The Management Company may decide to terminate the marketing arrangement in place in any given country in accordance with Article 93a of Directive 2009/65/EC.

Changes in exchange rates may cause the NAV per share in the investor's base currency to fluctuate.

Particular attention is paid to the contents of this document but no guarantee, warranty or representation, express or implied, is given to the accuracy, correctness or completeness thereof.

Prior to any transaction, clients should check whether it is suited to their personal situation, and analyse the specific risks incurred, especially financial, legal and tax risks, and consult professional advisers if necessary.

Please refer to the Key Investor Information Document and prospectus with special attention to the risk warnings before investing. This Sub-Funds are classified as art.8 and 9 SFDR. For further information on ESG, please refer to: https://www.ram-ai.com/en/regulatory-information and the relevant Sub-Fund webpage, section "Sustainability-related disclosures".

The prospectus, constitutive documents and financial reports are available in English and French while PRIIPs KID are available in the relevant local languages. These documents can be obtained, free of charge, from the SICAVs’ and Management Company’s head office and www.ram-ai.com, its representative and distributor in Switzerland, RAM Active Investments S.A. and the relevant local representatives in the distribution countries.

Issued in Switzerland by RAM Active Investments S.A. which is authorised and regulated in Switzerland by the Swiss Financial Market Supervisory Authority (FINMA). Issued in the European Union and the EEA by the authorised and regulated Management Company, Mediobanca Management Company S.A. 2 Boulevard de la Foire, 1528, Luxembourg, Grand Duchy of Luxembourg.

The source of the above-mentioned information (except if stated otherwise) is RAM Active Investments and the date of reference is the date of this document.

More News & insights

.png)

.png)

.png)