Risks Are Piling Up: Quality and Market-Neutral Strategies Attractive Again (en Anglais uniquement)

.png)

Liquidity Conditions are Deteriorating

The last few months have exposed clear cracks in the liquidity underpinning global markets, and this preceded the current war in Iran.

The most visible cracks have appeared in private credit, where a wave of defaults has revealed far more widespread fraudulent double-pledging of assets than previously thought, culminating in the recent string of suspensions of redemptions in ‘semi-liquid’ private credit funds.

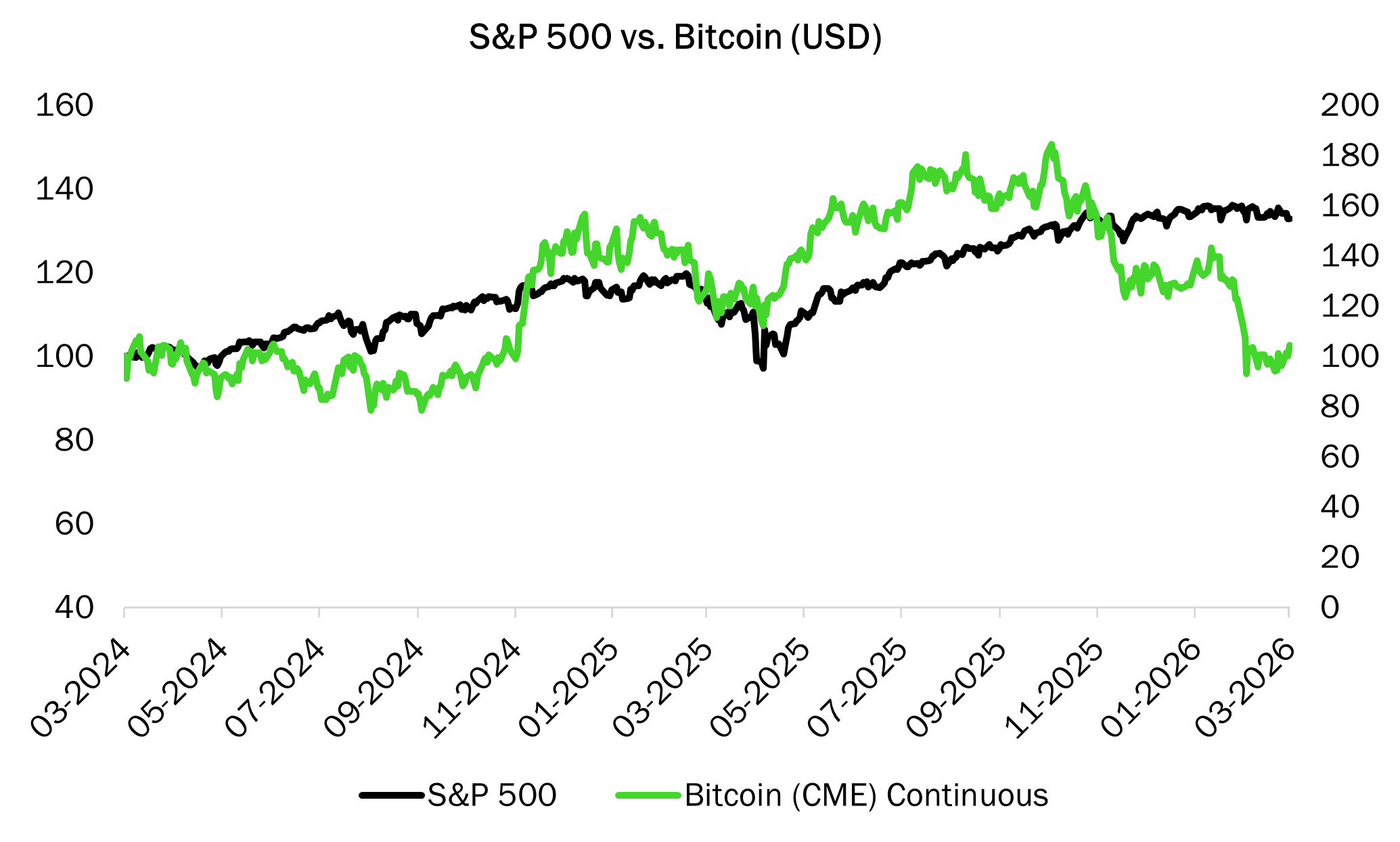

Crypto assets offer a complementary signal. Often a proxy for excess liquidity in the financial system, they have been unable to reclaim their highs even as the broad market rallied at the beginning of the year — another indication that the liquidity surplus is fading.

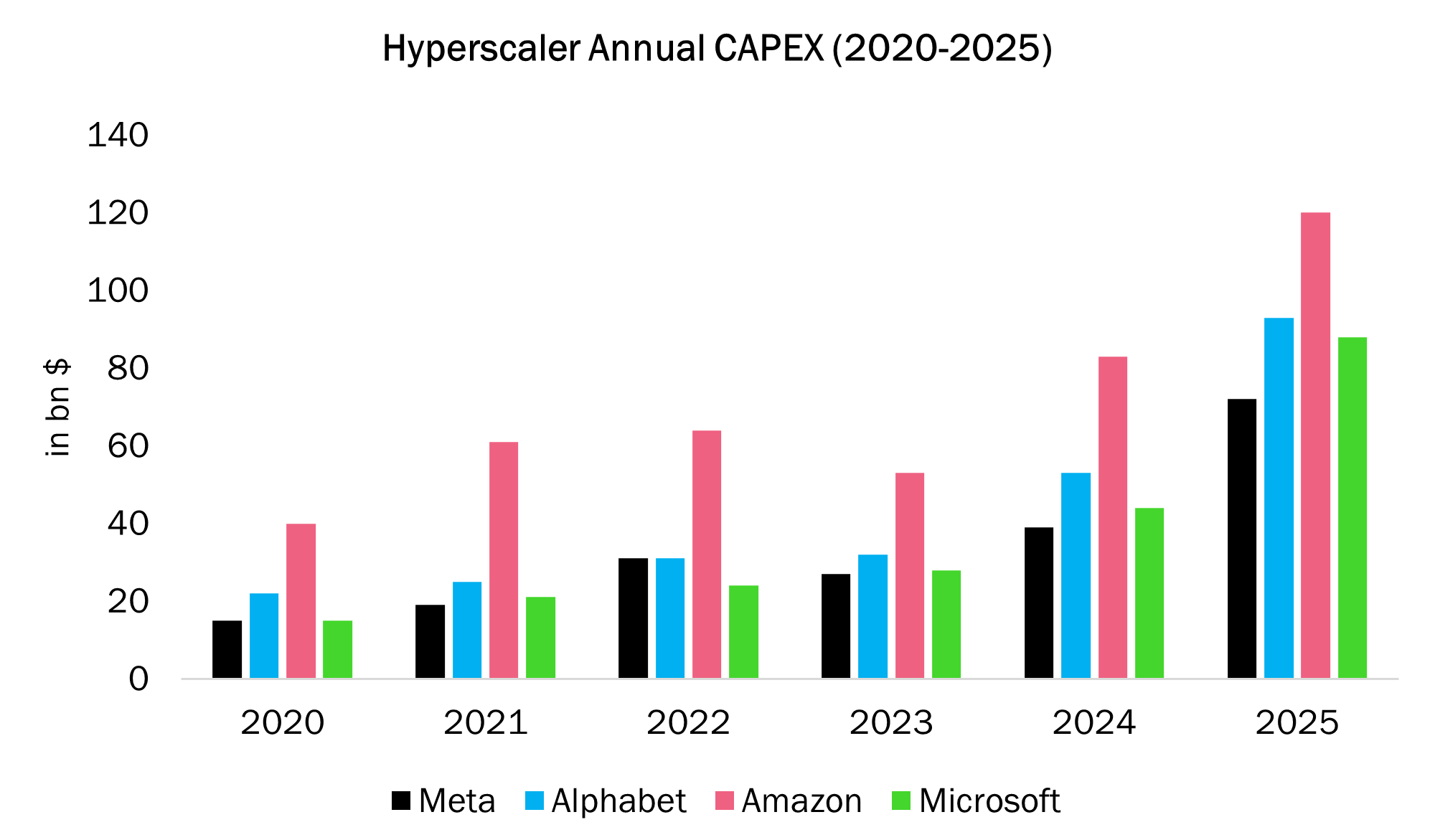

As equity investors, what has concerned us since the start of the year is the trajectory of mega-cap technology names — historically the largest providers of liquidity to financial markets through buybacks and dividends. Their free cash flow generation has melted away on the back of extraordinary capital expenditure to fund AI investments.

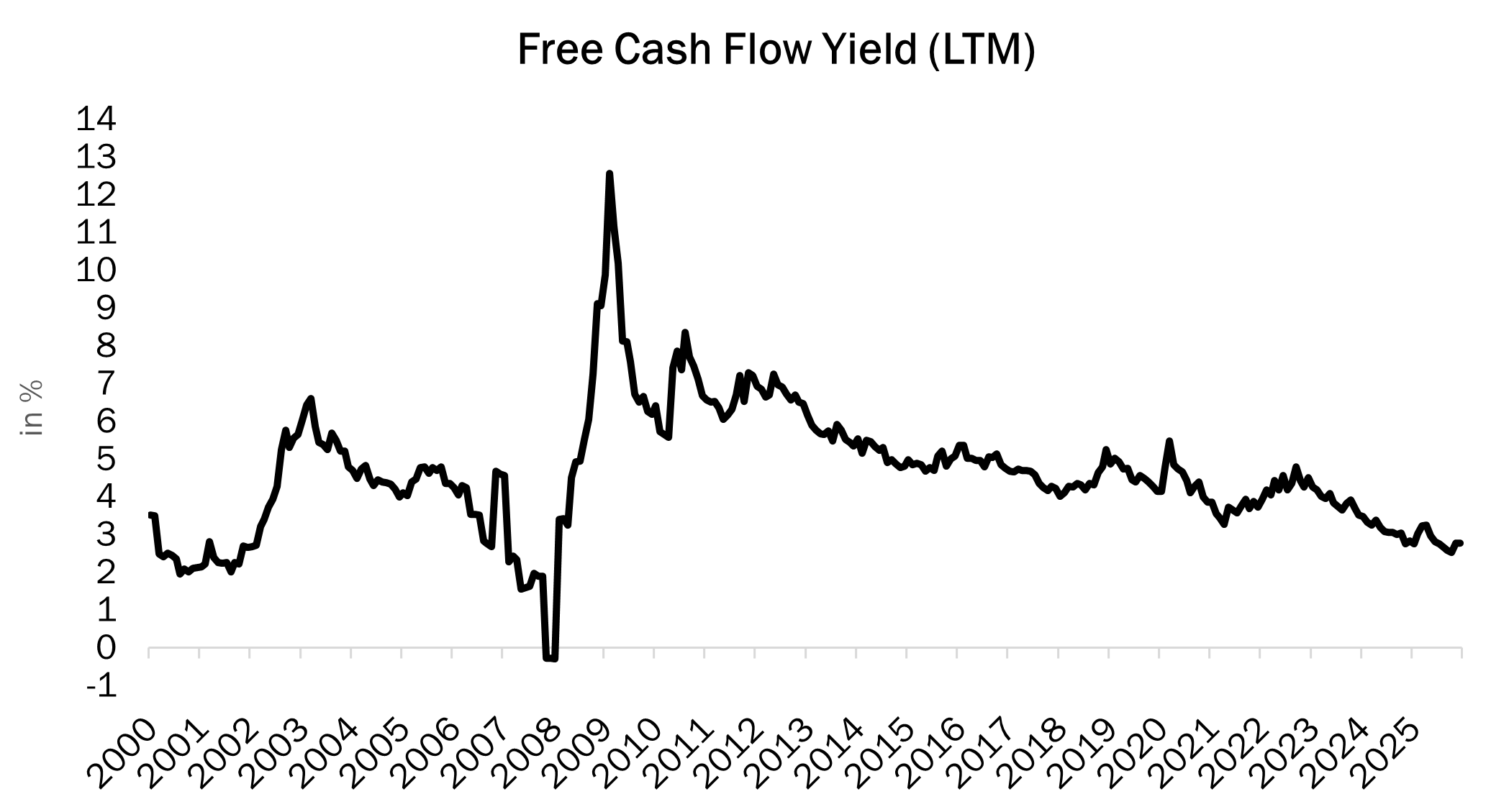

US equities now trade at more than 30 times free cash flow, implying a sub-3% free cash flow yield (see S&P 500 FCF yield chart below) — levels last seen during the tech bubble of the early 2000s.

The recent turmoil in the Middle East adds a further risk, potentially undermining one of the key lenders financing the AI expansion. Institutional Middle Eastern investors have poured tens of billions of dollars into private AI companies and hyperscalers; any pullback would tighten funding conditions further.

Against this backdrop of diminishing liquidity and with the recent increase of macroeconomic uncertainty with the Iran war, the downside risk in equities is rising, making the search for quality and diversification all the more important.

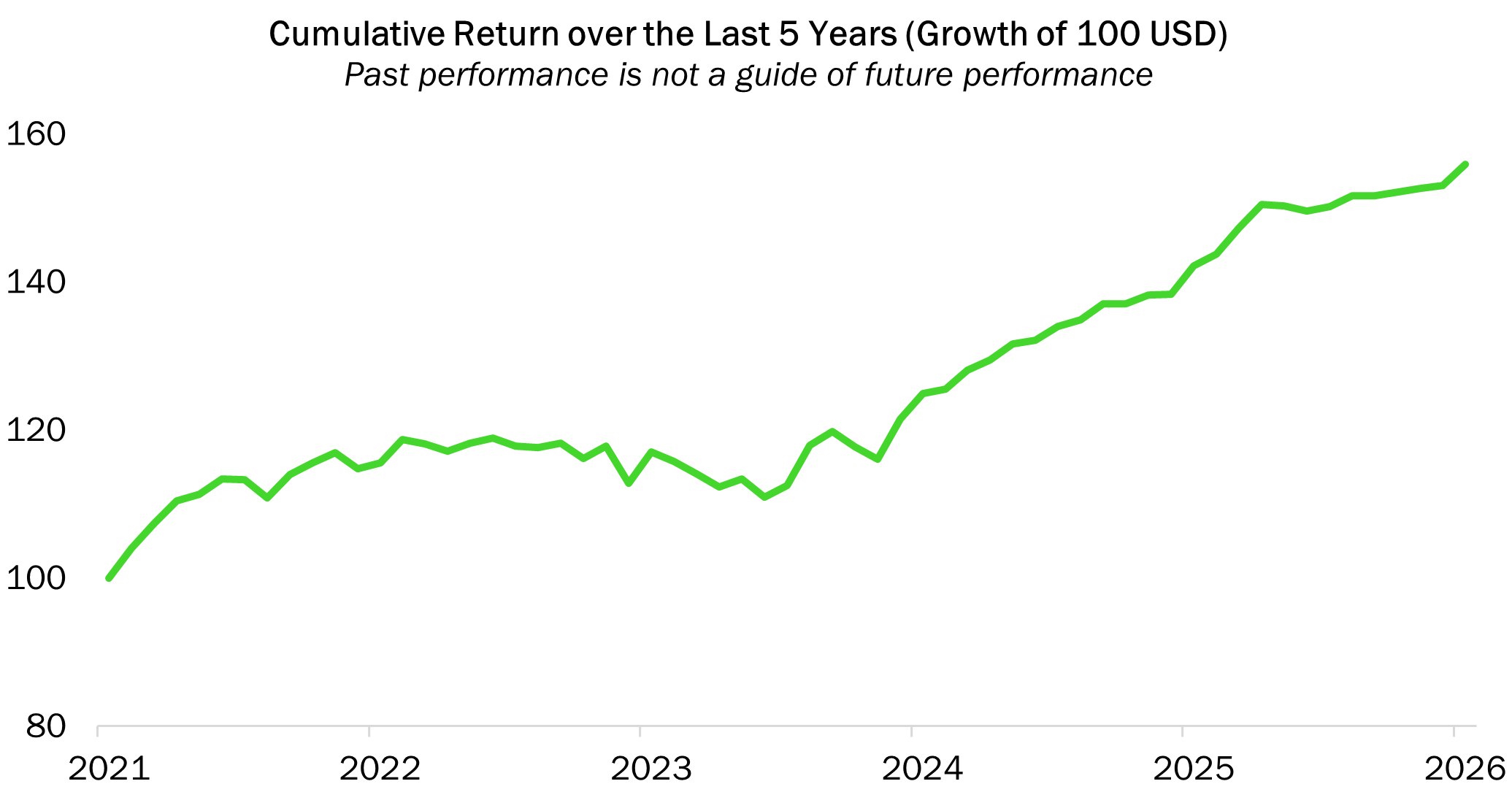

The RAM European Market Neutral Equity Fund is designed for this type of environment. By systematically exploiting value, quality, price, and liquidity-driven inefficiencies across European equities, while maintaining near-zero market exposure, the fund aims to deliver returns that are structurally decoupled from equity market direction. Its strong net long quality bias makes it well-suited for late-cycle phases, where quality spreads tend to widen as risk appetite diminishes. As illustrated in the cumulative return chart below, the fund has compounded steadily over the past five years, navigating both the 2022 drawdown environment and the 2024–2025 AI-driven equity rally without meaningful directional exposure.

The fund’s decorrelation from major asset classes is confirmed by its correlation matrix. Across equities and fixed income, correlations remain close to zero or negative, underscoring its value as a genuine diversifier in multi-asset portfolios.

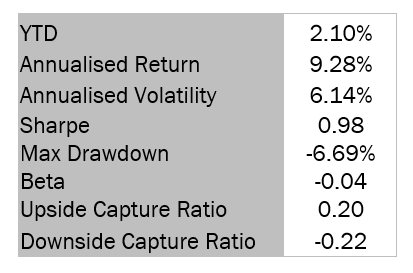

The fund (Share Class IH USD) is up 2.10% YTD, following robust calendar year returns of 10.40% in 2025 and more than 19% in 2024. The risk profile is equally compelling: an annualised Sharpe ratio close to 1.0, a maximum drawdown contained at -6.69%, and, critically, a negative downside capture ratio of -0.22, meaning the fund has historically gained during broad equity market declines. With a beta of -0.04, performance is almost entirely attributable to alpha generation rather than market directionality.

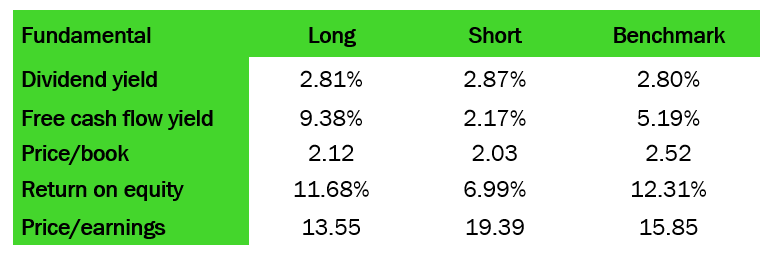

The portfolio’s quality construction is clearly reflected in its fundamental characteristics below. The long book exhibits a markedly superior free cash flow yield (9.38% vs. 2.17% for the short book), higher return on equity (11.68% vs. 6.99%), and lower price/earnings multiples (18.35x vs. 20.89x for the benchmark), a disciplined combination of quality at value. This structural long quality / short low-quality positioning is the engine behind the fund’s resilience. The statistical arbitrage allocation, scaled up in 2024, further diversifies the return sources and reinforces the fund’s robustness across market regimes.

Search for Convexity

The fund’s net long quality bias, expressed primarily through a systematic short of low-quality stocks, is designed to generate asymmetric returns during market stress. Low-quality stocks historically amplify their beta on the downside, turning the short book into an active source of performance precisely when equity markets deteriorate. This is not a passive hedge: it is a structural feature of the portfolio construction that becomes more valuable as the cycle turns.

Our statistical arbitrage strategy is intended to further improve the convex profile of the fund, as the strategy tends to perform well overall in high-volatility market regimes (best year for the strategy in the last cycle was 2020).

Zoom-in: Our Statistical Arbitrage sub-strategy could be a good reserve of performance over the next 12 months.

The statistical arbitrage book, representing 25% of the fund, has been a performance detractor over the past six months — a pattern consistent with the broader statistical arbitrage in the industry. The environment has been structurally hostile to mean-reversion strategies: relentless momentum, absent price dislocations, and no meaningful liquidity shocks have all compressed the opportunity set for contrarian, short-horizon signals.

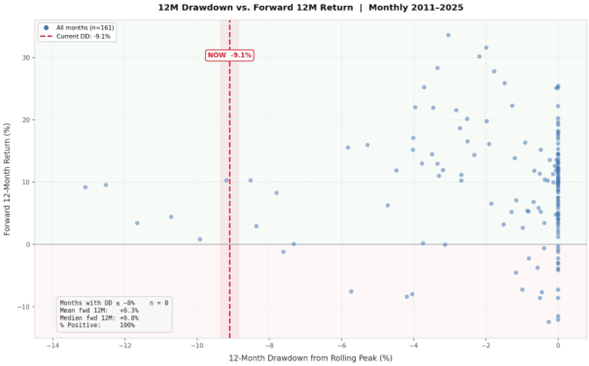

Yet this is precisely the context in which history favours patience. Momentum and mean-reversion strategies are structurally complementary — their correlation over time is low to slightly negative. Extended momentum regimes have historically created the conditions for sharp and profitable mean-reversion episodes. With daily rebalancing and a naturally convex return profile, the statistical arbitrage book is well positioned to capture these dislocations rapidly when they materialise. The past six months of underperformance are, in our view, a reserve of future performance — as the chart below illustrates.

Every episode of comparable drawdown depth (≤ -8%) within the Statistical Arbitrage Book since 2011 was followed by positive 12-month forward returns, with a median recovery of +6.3% and a 100% hit rate across 8 observations. The current -9.1% drawdown sits squarely within this historical context, suggesting the strategy’s mean-reverting properties are poised to reassert themselves.

Glossary

Capex (Capital Expenditure): Corporate spending on physical assets, technology, or infrastructure to expand operations or improve efficiency. Large capex announcements often initially boost stock prices but may lead to reversals if returns don’t materialise.

Equity Risk Premium: The extra return investors expect from stocks compared to risk-free government bonds. A negative equity risk premium indicates stocks offer lower expected returns than bonds—a warning sign of overvaluation.

Free Cash Flow Yield: The ratio of a company’s free cash flow to its market value, expressed as a percentage. Higher yields indicate better value; yields around 3% are historically low and suggest expensive valuations.

Market Neutral: An investment strategy that holds both long positions (buying stocks expected to rise) and short positions (selling stocks expected to fall) in equal measure, aiming to generate returns independent of overall market direction while maintaining near-zero market exposure.

Statistical Arbitrage: A quantitative trading strategy that exploits short-term pricing inefficiencies between related securities using statistical models. These strategies typically hold positions for brief periods and profit from mean reversion or temporary mispricings.

Deep Learning: Advanced artificial intelligence techniques that use neural networks with multiple layers to analyse complex patterns in large datasets. In investment management, deep learning helps identify non-linear relationships and market inefficiencies that traditional models may miss.

Sharpe Ratio: A risk-adjusted return metric that compares a fund’s excess return (above the risk-free rate) to its volatility. A higher Sharpe Ratio suggests better return per unit of risk taken.

Beta: A measure of a fund’s sensitivity to market movements. A beta of 1 means the fund moves in line with the market; below 1 indicates lower sensitivity, while above 1 indicates higher sensitivity. Negative beta means the fund moves opposite to the market.

Alpha: A measure of a fund’s excess return relative to its benchmark. Positive alpha indicates the fund outperformed the benchmark after adjusting for market risk, reflecting manager skill or effective strategy execution.

Upside Capture Ratio: Shows how well a fund captures gains when the market is rising. A ratio of 1.0 (or 100%) means the fund matches the market during up periods; above 1.0 means outperformance.

Downside Capture Ratio: Shows how much of the market’s losses a fund experiences when markets decline. A ratio below 1.0 (or 100%) means the fund loses less than the market during down periods—a key indicator of defensive strength and risk management.

Image Gallery

Legal Disclaimer

The fund is a Sub-Funds of RAM (Lux) Systematic Funds, a Luxembourg SICAVs with registered office: 14, Boulevard Royal L-2449 Luxembourg, approved by the CSSF and constituting a UCITS (Directive 2009/65/EC). This marketing document is only provided for information purposes to professional clients, and it does not constitute an offer, investment advice or a solicitation to subscribe shares in any jurisdiction where such an offer or solicitation would not be authorised or it would be unlawful. In particular, the Funds are not offered for sale in the United States or its territories and possessions, nor to any US Person (citizens or residents of the United States of America). Note to investors domiciled in Singapore: shares of the Sub-Fund offered in Singapore are restricted schemes under the Sixth Schedule to the Securities and Futures (Offers of Investments) (Collective Investment Schemes) Regulations of Singapore. This document is confidential and is intended only for the use of the person to whom it was delivered; it may not be reproduced or distributed. There is no guarantee that the holdings shown will be held in the future. The investment described concerns the acquisition of shares in the Sub-Fund and not in a specific underlying asset. Past performance is not a guide to current or future results. There is no guarantee to get back the full amount invested. The performance data do not take into account fees and expenses charged on subscription and redemption of shares nor any taxes that may be levied. As a subscription fee calculation example, if an investor invests EUR 1000 in a fund with a subscription fee of 5%, the investor will pay to his financial intermediary EUR 47.62 on the investment amount, resulting with a subscribed amount of EUR 952.38 in fund shares. In addition, potential account keeping costs (by investor’s custodian) may reduce the performance. Some shares in the Sub-Fund may apply a performance fee. Please refer to the section ‘Fees and Charges’ and to the ‘Glossary’ in this document for further details. Leverage intensifies the risk of potential increased losses or returns. RAM Active Investments may decide to terminate the marketing arrangement in place in any given country in accordance with Article 93a of Directive 2009/65/EC. Changes in exchange rates may cause the NAV per share in the investor’s base currency to fluctuate. Particular attention is paid to the contents of this document but no guarantee, warranty or representation, express or implied, is given to the accuracy, correctness or completeness thereof. Prior to any transaction, clients should check whether it is suited to their personal situation, and analyse the specific risks incurred, especially financial, legal and tax risks, and consult professional advisers if necessary. Please refer to the Key Investor Information Document and prospectus with special attention to the risk warnings before investing. For further information on ESG, please refer to https://www.ram-ai.com/en/regulatory-information and the relevant Sub-Fund webpage. The prospectus, constitutive documents and financial reports are available in English and French while KIIDs are available in the relevant local languages. These documents can be obtained, free of charge, from the SICAVs’ and Management Company’s head office and www.ram-ai.com, its representative and distributor in Switzerland, RAM Active Investments S.A. and the relevant local representatives in the distribution countries. A summary of Investors’ rights is available on: https://www.ram-ai.com/en/regulatory-information Issued in Switzerland by RAM Active Investments S.A. which is authorised and regulated in Switzerland by the Swiss Financial Market Supervisory Authority (FINMA). Issued in the European Union and the EEA by the authorised and regulated Management Company, Mediobanca Management Company SA, 2 Boulevard de la Foire 1528 Luxembourg, Grand Duchy of Luxembourg. The source of the above-mentioned information (except if stated otherwise) is RAM Active Investments SA and the date of reference is the date of this document, end of the previous month.

Plus d'actualités et d'informations

.png)

.png)