2026 Equity Outlook: The Case for Cash Flow Quality

.png)

For professional investors only - Marketing Material

A defining equity theme for 2026 is the widening disconnect between market valuations and realised cash-flow generation. This divergence is largely fueled by a massive acceleration in AI-driven capital expenditures, which is currently weighing on near-term liquidity despite long-term growth promises.

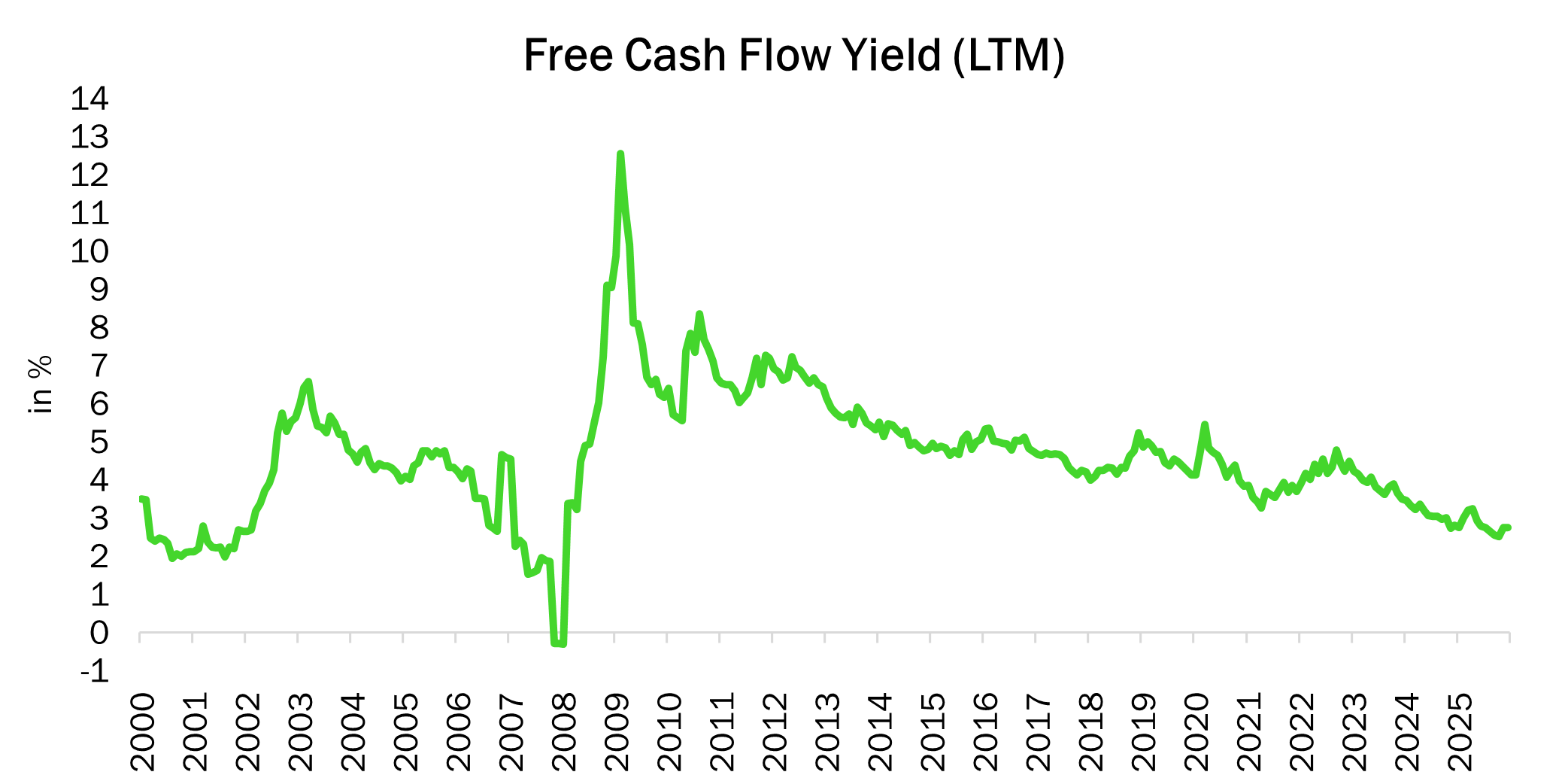

Evidence of this valuation gap is clearest in the S&P 500 free cash-flow yield, which has now dipped below the 3% threshold. Approaching historical lows, this compression highlights the premium investors are currently paying for future AI-driven growth at the expense of immediate cash returns.

In parallel, the Hyperscaler Annual CAPEX chart highlights a sharp and sustained increase in investment spending by U.S. technology leaders. Hyperscalers—the dominant cloud and data providers like Amazon, Alphabet, Meta, and Microsoft—serve as the primary architects of the AI ecosystem, providing the massive computing power required to train and run large-scale models. Monitoring their spending is critical because the financing of this cycle has reached a structural turning point. As collective spending scales toward $600 billion in 2026, the AI supercycle is increasingly being fueled by debt. For the first time, these traditionally cash-rich giants are becoming major issuers in the corporate bond market to sustain their aggressive investment pace, marking a departure from the self-funded growth models that defined the previous decade.

.png)

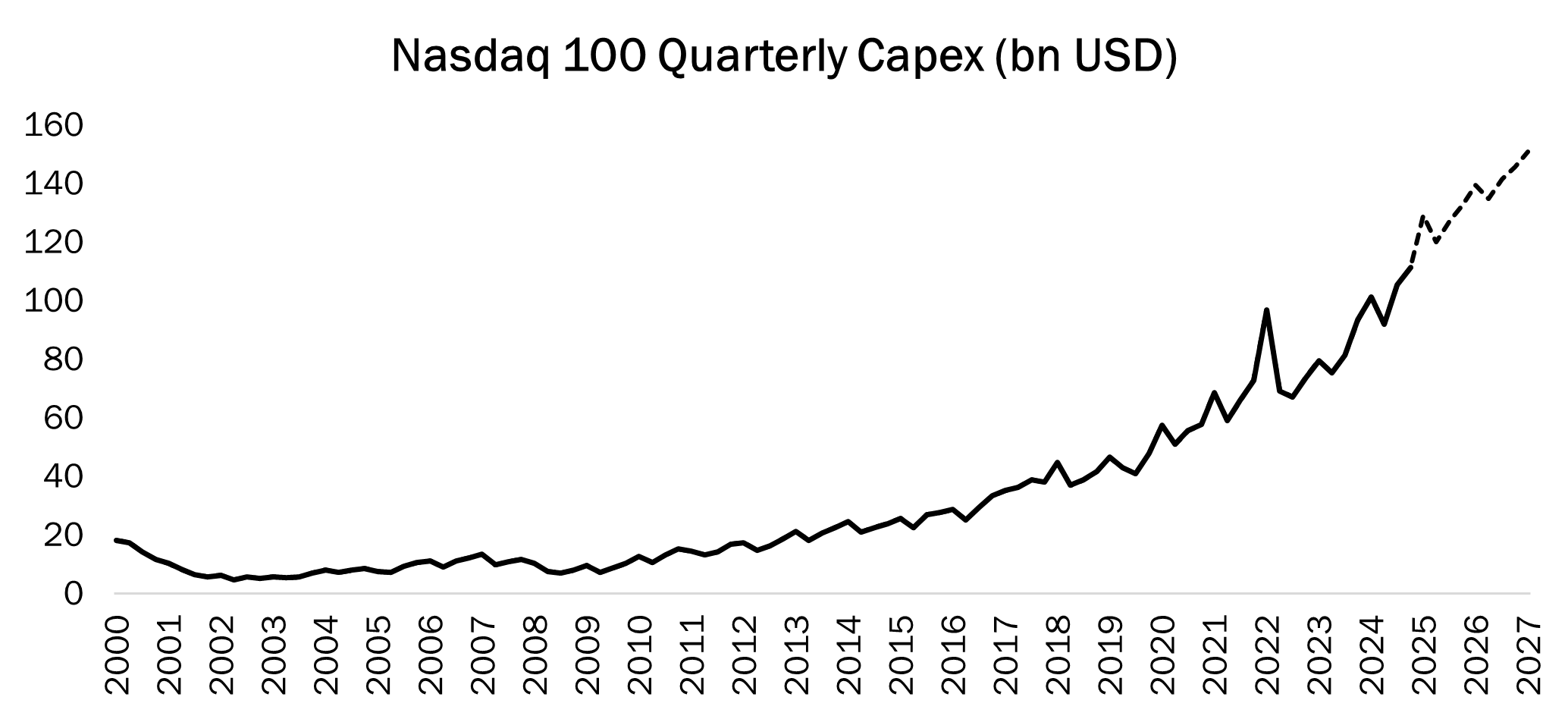

The Nasdaq 100 Quarterly Capex chart underscores the unprecedented scale of the current investment cycle, showing that quarterly outlays have shifted from a steady twenty-year climb into a near-vertical acceleration beginning in late 2023.

This confluence of stretched valuations and rising capital intensity—now increasingly fueled by debt—fundamentally alters the equity risk profile for 2026. As hyperscalers pivot from self-funded growth to becoming major corporate bond issuers, market fragility increases; the index-level safety net of net-cash balance sheets is thinning. This shift leaves the market uniquely vulnerable to liquidity constraints or earnings disappointments, particularly if the 'monetisation gap' persists and the high-conviction AI narrative fails to deliver immediate, bottom-line results. In the current environment, where the S&P 500 free cash-flow yield is at its lowest level since 2008, the priority is to gain exposure to high-quality companies—those with strong free cash-flow generation and solid balance sheets, able to withstand downturns. Such companies tend to offer better downside protection in the event of market correction.

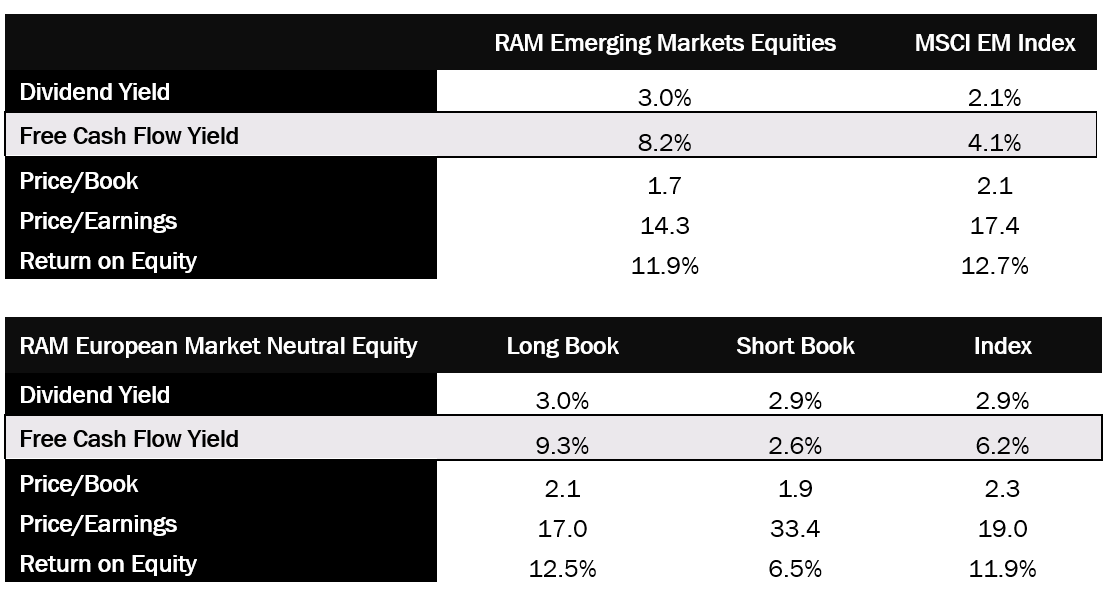

The RAM Emerging Markets Equities Fund may offer a strategic solution for diversifying away from U.S. equities and capturing the long-term growth potential of emerging markets. Utilising a systematic, quality-focused approach, the fund targets firms with high free cash-flow generation and robust balance sheets—qualities that are increasingly valuable in the current market environment. This disciplined selection process creates a convex return profile relative to the MSCI Emerging Markets Index. Over the long term, the strategy aims to deliver an upside capture ratio of 1.0 while limiting the downside capture ratio to 0.7, with the objective of providing investors with full participation in market gains while significantly cushioning the impact of drawdowns.

In parallel, the RAM European Market Neutral Equity Fund may be well suited for investors seeking to decorrelate from equity markets. By neutralising market exposure, the fund maintains a near-zero beta, offering a performance profile that is largely independent of overall market direction and driven primarily by single-stock alpha. This focus on stock-specific returns allows the strategy to serve as a stabilising element in an equity outlook defined by valuation disconnects and increased market fragility.

Together, these two strategies provide an effective combination through their focus of return potential and risk control by placing fundamental quality at the core of the investment process. As illustrated in the tables below, both funds maintain a significant cash-flow advantage over their respective markets—with the emerging markets strategy delivering an 8.2% free cash-flow yield and the European market neutral strategy's long book reaching 9.3%. By prioritising firms with robust balance sheets and superior cash generation, this dual approach is designed to navigate the current market fragility while capturing high-conviction opportunities.

The 2026 outlook is defined by a critical pivot: a transition into a 'debt-fueled' era as the AI supercycle enters its most capital-intensive phase. With hyperscaler capex now consistently outpacing near-term internal cash flow, the traditional 'cash machine' profile of U.S. technology leaders is being tested by massive, front-loaded investments. To navigate this environment, strategic reallocation is essential. By rotating toward regions with more attractive cash-flow yields—particularly emerging markets—and complementing directional exposure with market-neutral strategies, investors can maintain equity participation while reducing dependence on capital-intensive growth segments. This dual approach aims to neutralise the risks of high leverage and valuation disconnects, significantly improving overall portfolio resilience.

Image Gallery

Legal Disclaimer

Important Information:

RAM (LUX) Systematic Funds – Emerging Markets Equities Fund and RAM (LUX) Systematic Funds – European Market Neutral Equity Fund are Sub-Funds of RAM (Lux) Systematic Funds, a Luxembourg SICAV with registered office: 14, Boulevard Royal L-2449 Luxembourg, approved by the CSSF and constituting a UCITS (Directive 2009/65/EC). Mediobanca Management Company S.A. 2 Boulevard de la Foire 1528, Luxembourg, Grand Duchy of Luxembourg is the Management Company.

The information and analyses contained in this document are based on sources deemed to be reliable. However, RAM Active Investments S.A. cannot guarantee that said information and analyses are up-to-date, accurate or exhaustive, and accepts no liability for any loss or damage that may result from their use. All information and assessments are subject to change without notice.

This document has been drawn up for information purposes only. It is neither an offer nor an invitation to buy or sell the investment products mentioned herein and may not be interpreted as an investment advisory service. It is not intended to be distributed, published or used in a jurisdiction where such distribution, publication or use is forbidden, and is not intended for any person or entity to whom or to which it would be illegal to address such a document. In particular, the investment products are not offered for sale in the United States or its territories and possessions, nor to any US person (citizens or residents of the United States of America). The opinions expressed herein do not take into account each customer’s individual situation, objectives or needs. Customers should form their own opinion about any security or financial instrument mentioned in this document. Prior to any transaction, customers should check whether it is suited to their personal situation, and analyse the specific risks incurred, especially financial, legal and tax risks, and consult professional advisers if necessary.

Not all share classes in the Sub-Fund are registered in all countries.

Note to investors domiciled in Singapore: shares of the Sub-Fund offered in Singapore are restricted schemes under the Sixth Schedule to the Securities and Futures (Offers of Investments) (Collective Investment Schemes) Regulations of Singapore.

There is no guarantee that the holdings shown will be held in the future. The investment described concerns the acquisition of shares in the Sub-Fund and not in a specific underlying asset. Past performance is not a guide to current or future results. There is no guarantee to get back the full amount invested. The performance data do not take into account fees and expenses charged on subscription and redemption of shares nor any taxes that may be levied. The Management Company may decide to terminate the marketing arrangement in place in any given country in accordance with Article 93a of Directive 2009/65/EC. Leverage intensifies the risk of potential increased losses or returns. Changes in exchange rates may cause the NAV per share in the investor's base currency to fluctuate.

Please refer to the Key Information Document and prospectus with special attention to the risk warnings before investing. For further information on ESG, please refer to https://www.ram-ai.com/en/regulatory-information and the relevant Sub-Fund webpage. The prospectus, constitutive documents and financial reports are available in English and French while KIDs are available in the relevant local languages. These documents can be obtained, free of charge, from the SICAVs’ and Management Company’s head office and www.ram-ai.com, its representative and distributor in Switzerland, RAM Active Investments S.A. and the relevant local representatives in the distribution countries.

This marketing document has not been approved by any financial Authority. A summary of Investors’ rights is available on: https://www.ram-ai.com/en/regulatory-information

This document is strictly confidential and addressed solely to its intended recipient; its reproduction and distribution are prohibited. It has not been approved by any financial Authority. Issued in Switzerland by RAM Active Investments S.A. (Rue du Rhône 8 CH-1204 Geneva) which is authorised and regulated in Switzerland by the Swiss Financial Market Supervisory Authority (FINMA). Issued in the European Union and the EEA by the authorised and regulated Management Company, Mediobanca Management Company S.A. , 2 Boulevard de la Foire 1528 Luxembourg, Grand Duchy of Luxembourg. The source of the above-mentioned information (except if stated otherwise) is RAM Active Investments and the date of reference is the date of this document.

No part of this document may be copied, stored electronically or transferred in any way, whether manually or electronically, without the prior agreement of RAM Active Investments S.A. and Mediobanca Management Company S.A

Swiss Representative: Swiss Paying Agent:

RAM Active Investments S.A. CACEIS Bank, Montrouge, succursale de Nyon/Suisse

Rue du Rhône 8 Route de Signy 35

CH-1204 Genèva CH-1260 Nyon

More News & insights

.png)

.png)