2026 Credit Insights: Balancing Risk and Reward

.png)

For professional investors only - Marketing Material

Credit markets have continued to perform strongly in 2025. Spreads rebounded swiftly from the weakness seen around ‘Liberation Day’ and have tightened steadily since the spring.

Looking ahead to 2026, a key question is whether US growth can remain resilient in the face of weakening underlying trends—most notably slower job creation—while the euro area appears set for a clearer upswing. Euro area Gross Domestic Product (GDP) growth is expected to accelerate into late 2026, reaching 1.4% year-on-year by Q4,* supported by fiscal stimulus and stronger domestic demand.

* Data as of 31st December 2025

Fundamentals Remain a Pillar of Strength

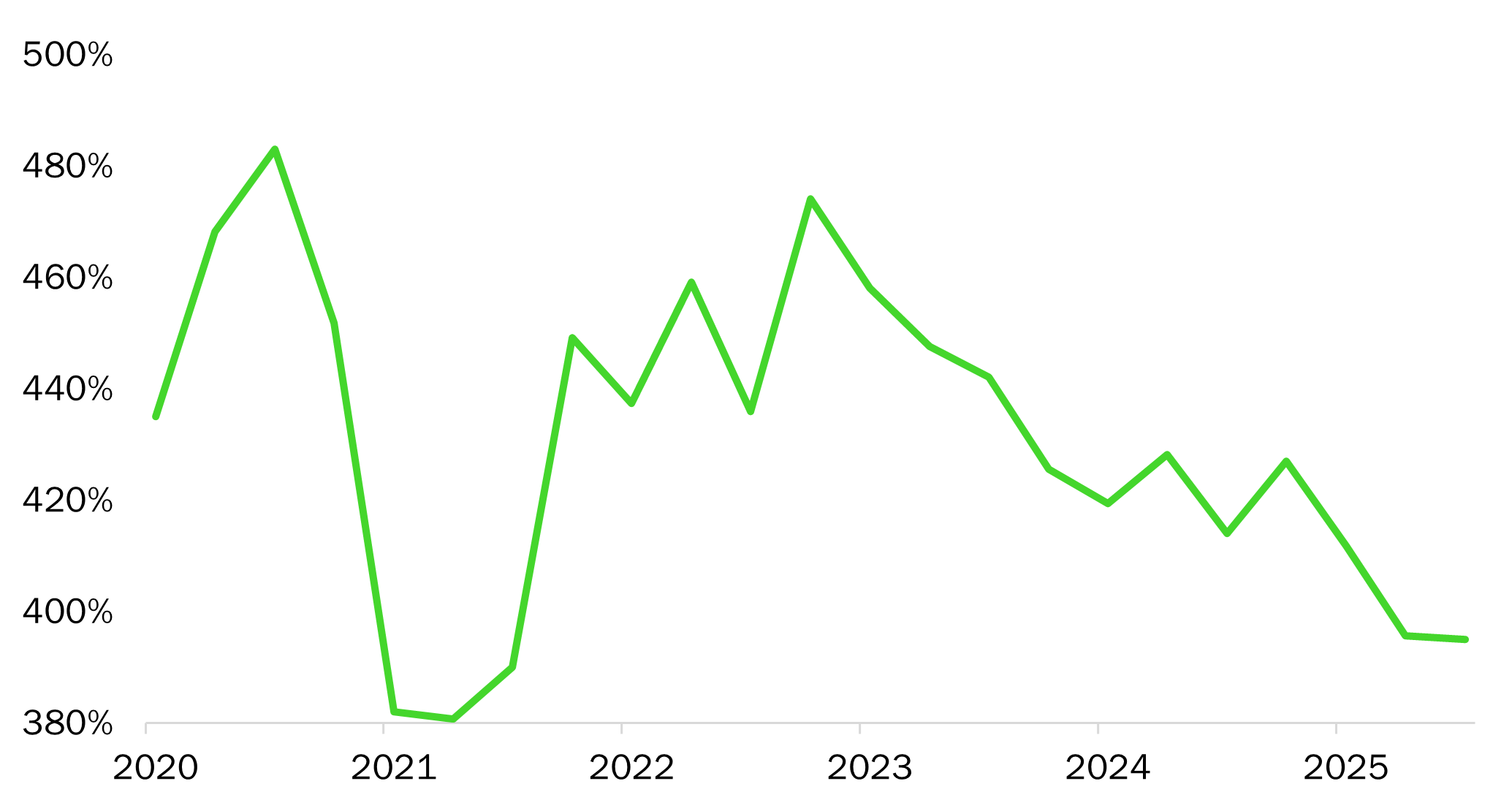

Corporate fundamentals remain broadly supportive. In 2025, issuers have experienced positive credit migration, stronger balance sheet metrics, and higher interest coverage, signalling reduced vulnerability relative to prior cycles. Indeed, a greater number of companies have seen their credit quality improve rather than deteriorate. These trends underpin ongoing issuance and provide resilience against macroeconomic volatility. Notably, leverage among European high-yield issuers has been trending lower since Q4 2022 and now sits at the bottom of the current economic cycle.

Leverage evolution for European High-yield issuers

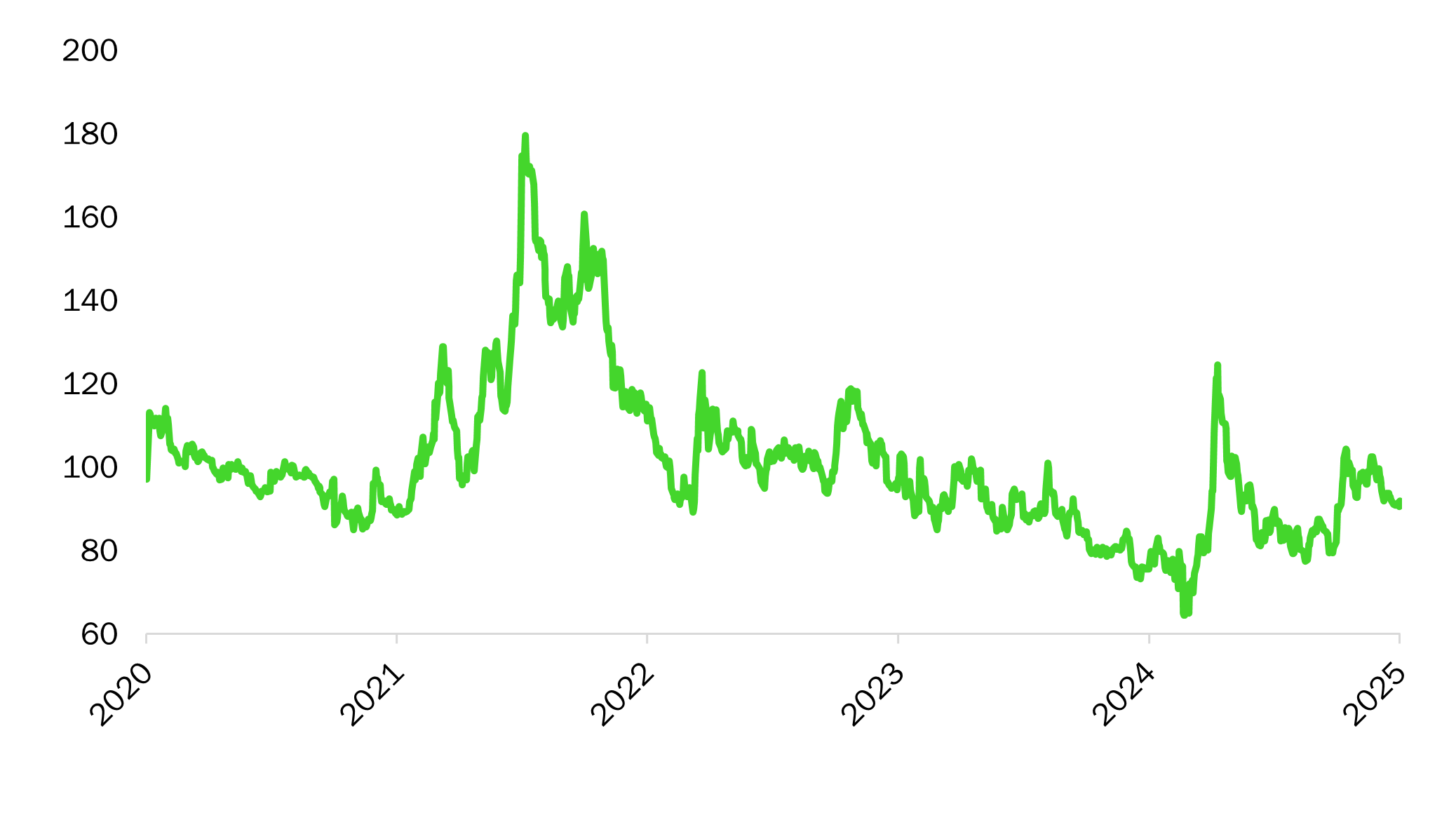

With global GDP expected to grow, banks well-capitalised, corporates generally healthy, and households relatively resilient, we believe the current cycle is likely to extend. Although spreads on European high-yield bonds are approaching the lowest levels of the past five years, they may still tighten further, supported by the lower indebtedness of the underlying borrowers.

Spread per turn of leverage in European High-yield

Spread compression appears less pronounced when adjusted for credit quality. When adjusted for leverage, valuations show a much shallower decline, particularly since the start of the earnings season in October. This suggests that spreads can tighten further before reaching the levels seen at the beginning of 2025.

Opportunities and Risks in the Year Ahead

While volatility may rise relative to 2025, our outlook for credit remains constructive heading into 2026. That said, the market is not without risk. While higher-quality segments have performed well, weaker credits continue to face pressure from a combination of issuer-specific and sector-wide challenges. The chemicals sector illustrates this divergence, with many issuers struggling amid excess supply from China and subdued demand from key end markets such as autos and housing.

This environment heightens the importance of active credit selection. Focusing on issuers with strong interest coverage, conservative balance sheets, and resilient cash flows should help improve risk-adjusted outcomes. We continue to see higher quality corporate and Collateralised Loan Obligation (CLOs) as offering some of the best potential risk-adjusted returns, but we prefer to be positioned further up the ratings curve and in higher quality issuers. We expect performance to be driven by elevated carry and yields in the context of strong technical drivers.

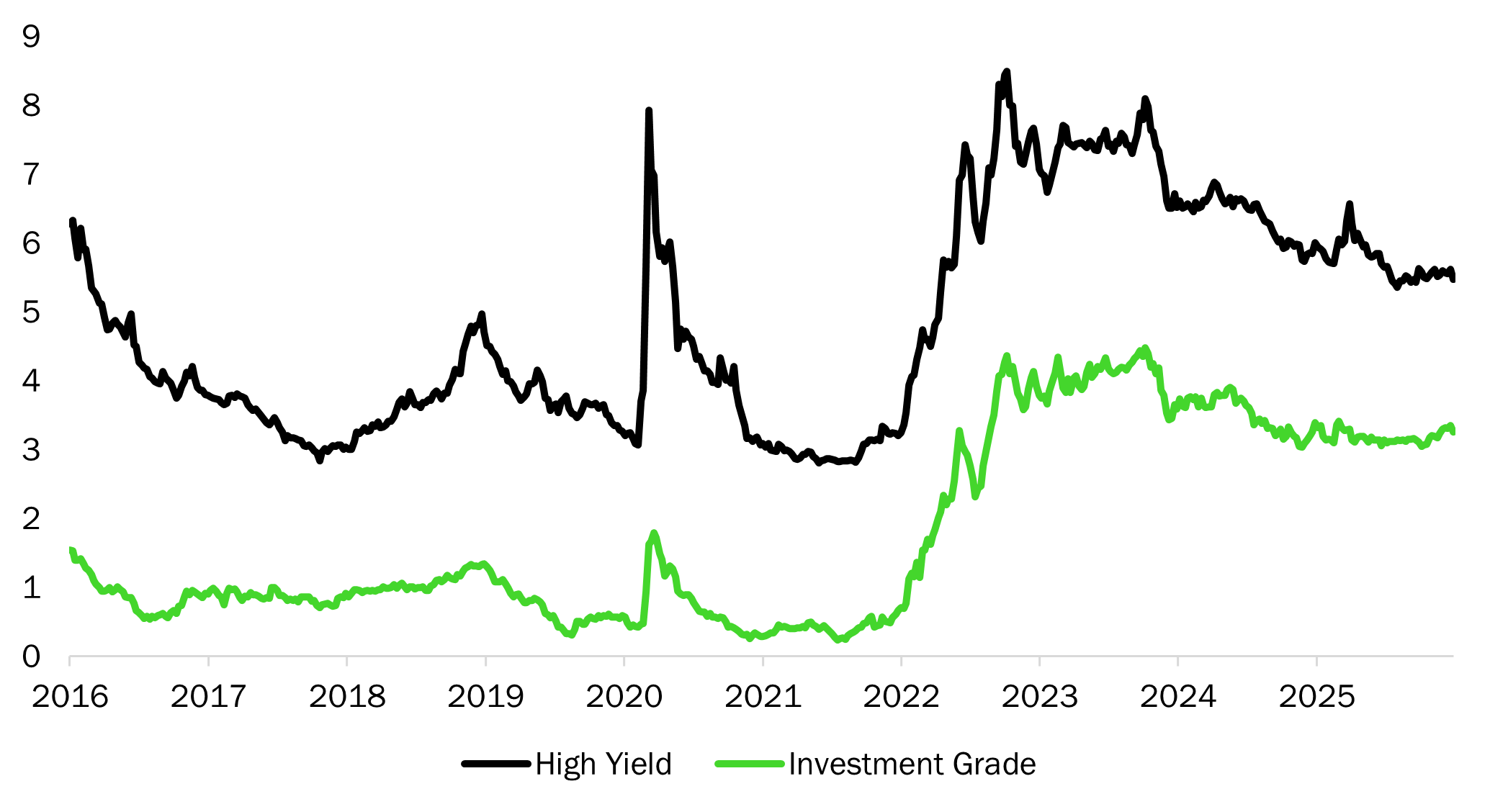

Despite tight spreads, overall yields remain healthy

Image Gallery

Legal Disclaimer

This document has been drawn up for information purposes only. It is neither an offer nor an invitation to buy or sell the investment products mentioned herein and may not be interpreted as an investment advisory service. It is not intended to be distributed, published or used in a jurisdiction where such distribution, publication or use is prohibited, and is not intended for any person or entity to whom or to which it would be illegal to address such a document. In particular, the products mentioned herein are not offered for sale in the United States or its territories and possessions, nor to any US person (citizens or residents of the United States of America). The opinions expressed herein do not take into account each customer’s individual situation, objectives or needs. Customers should form their own opinion about any security or financial instrument mentioned in this document. Prior to any transaction, customers should check whether it is suited to their personal situation and analyse the specific risks incurred, especially financial, legal and tax risks, and consult professional advisers if necessary. The information and analyses contained in this document are based on sources deemed to be reliable. However, RAM AI cannot guarantee that said information and analyses are up-to-date, accurate or exhaustive, and accepts no liability for any loss or damage that may result from their use. All information and assessments are subject to change without notice. Investors are advised to base their decision whether or not to invest in fund units on the most recent reports and prospectuses. These contain further information on the products concerned. The value of units and income thereon may rise or fall and is in no way guaranteed. The price of the financial products mentioned in this document may fluctuate and drop both suddenly and sharply, and it is even possible that all money invested may be lost. If requested, RAM AI will provide customers with more detailed information on the risks attached to specific investments. Exchange rate variations may also cause the value of an investment to rise or fall. Whether real or simulated, past performance is not necessarily a reliable guide to future performance.This marketing document has not been approved by any financial Authority, it is confidential and its total or partial reproduction and distribution are prohibited.

Plus d'actualités et d'informations

.png)

.png)