Commentaries

18 March 2019

February 2019 - When market excesses create opportunities for our strategies… - Systematic Fund Manager's Comments

1. From Deleveraging to Low Quality Rally is not an unseen situation on markets and generally leads to positive return for our Long Short strategies…

Global equity markets have experienced two distinct phases over the last 6 months, which proved to be challenging for fundamental stock pickers. The first part (October & November), was characterized by heightened volatility and a deleveraging phase during which both gross and net exposures were quickly and significantly reduced by the investment funds community. The second part (January & February), the market’s behavior was highly unselective, with “low-quality” stocks bought at the expense of “quality” ones in a short covering mood!

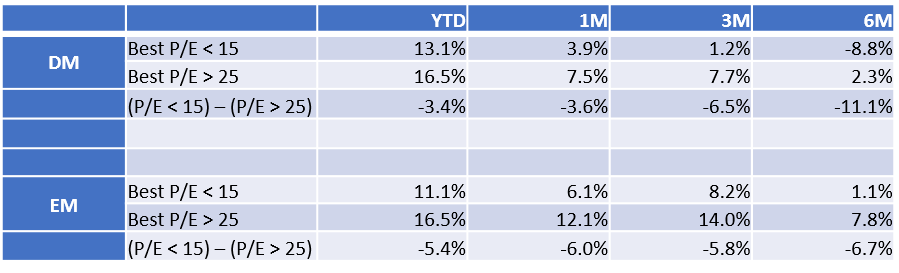

High P/E Outperforming Low P/E Stocks

The below table considers the Best P/E metrics across regions by filtering stocks with below 15x P/E versus those above 25x. The performance divergence between the two is significant. In other words, the momentum and fundamentals-agnostic trade has continued to work well globally, supported by central banks’ accommodative action.

Source: Bloomberg & RAM Active Investments. Filters applied: market cap > $1bn, as at 7th March 2019

The current period we find ourselves in is particularly brutal with little fundamental foundation for stock performance. However, this type of technical setup is relatively common following the end of a major trend and subsequent bounce in the underlying market. The consequence? The inefficiencies we aim to capture across small, mid, and large caps as well as Value, Low-Risk and Growth/Momentum investment styles are significant today. If history is any guide to the future, earnings cycle and company fundamentals should eventually prevail, and this could occur sooner rather than later given the extent of the divergence.

We have previously witnessed similarly challenging market conditions, and this has not altered our long-term excess return objectives. Interestingly, our research and experience indicate that following periods such as these, both our long and short engines can generate significant alpha and we have been quick to recover losses as markets display a high degree of dispersion.

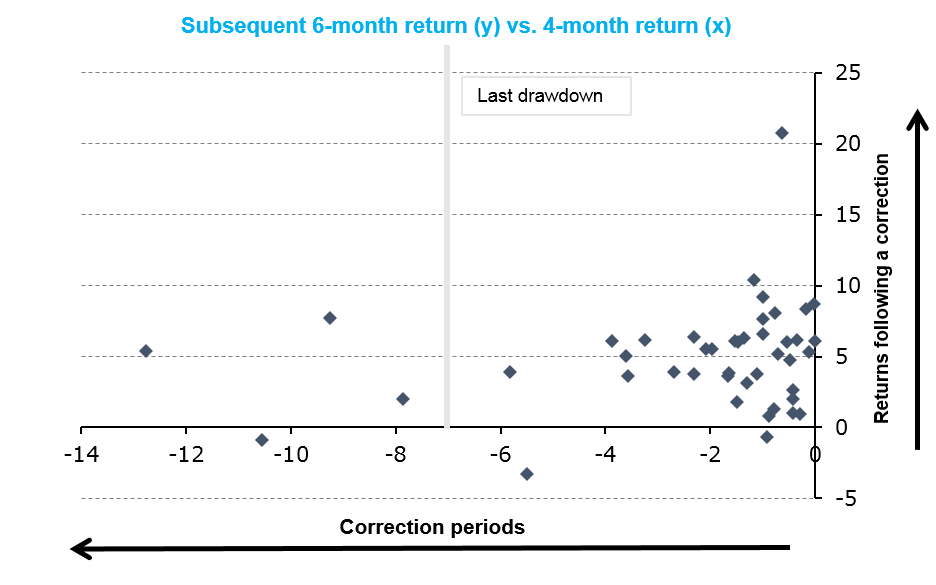

Whenever we’ve observed 6 months of negative cumulative returns on our Long/Short European Equity Fund, our average cumulative returns have been +3.2% over the following 3 months, and +5.1% over the following 6 months (see chart below).

Important Note: Prior to March 2009, performances are based on a back-test calculated on a hypothetical model. The Back-test performance is calculated using sub-strategies returns calculated based on simulated model portfolios rebalanced monthly on RAM equity investment screenings. The defined allocation of sub-strategies on the long and short side may not represent the exact contribution of strategies in real portfolio. After March 2009, RAM Long/Short European Equities Strategy shows performance net of fee of the RAM L/S European Equities Fund Class-I from December 2011 (1.5% of management fee+20% of performance fee) and of the RAM Absolute Return Fund prior to December 2011. The RAM Absolute Return Fund followed the same exact investment strategy within a Cayman vehicle (1.75% of Management fee+20% of performance fee) before it was converted to a UCITS.

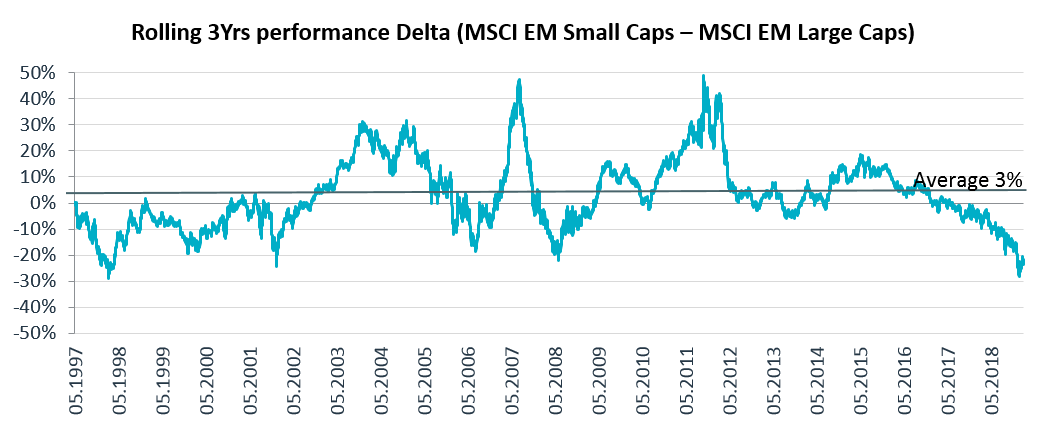

2. When markets ignore value on small caps in EM

Over the past 3-years, the herd mentality of investors has favoured large over small caps in emerging markets to a degree that has hitherto been unseen since the 1998 Asian Financial Crisis. History tells us that this situation represents an attractive entry point for investors looking for a true all-cap approach to investing in the region. Given the increased likelihood of a positive trend reversal of small and mid-caps relative to their large cap counterparts in the coming quarters, we believe our All-caps Strategy is well positioned to produce significant outperformance and to create diversification.

Source: RAM Active Investments as of 28.02.2019, MSCI indices

Direct access per fund to our latest Fund Manager's Comments:

Legal Disclaimer

This document has been drawn up for information purposes only. It is neither an offer nor an invitation to buy or sell the investment products mentioned herein and may not be interpreted as an investment advisory service. It is not intended to be distributed, published or used in a jurisdiction where such distribution, publication or use is prohibited, and is not intended for any person or entity to whom or to which it would be illegal to address such a document. In particular, the products mentioned herein are not offered for sale in the United States or its territories and possessions, nor to any US person (citizens or residents of the United States of America). The opinions expressed herein do not take into account each customer’s individual situation, objectives or needs. Customers should form their own opinion about any security or financial instrument mentioned in this document. Prior to any transaction, customers should check whether it is suited to their personal situation and analyse the specific risks incurred, especially financial, legal and tax risks, and consult professional advisers if necessary. The information and analyses contained in this document are based on sources deemed to be reliable. However, RAM AI Group cannot guarantee that said information and analyses are up-to-date, accurate or exhaustive, and accepts no liability for any loss or damage that may result from their use. All information and assessments are subject to change without notice. Investors are advised to base their decision whether or not to invest in fund units on the most recent reports and prospectuses. These contain further information on the products concerned. The value of units and income thereon may rise or fall and is in no way guaranteed. The price of the financial products mentioned in this document may fluctuate and drop both suddenly and sharply, and it is even possible that all money invested may be lost. If requested, RAM AI Group will provide customers with more detailed information on the risks attached to specific investments. Exchange rate variations may also cause the value of an investment to rise or fall. Whether real or simulated, past performance is not necessarily a reliable guide to future performance. The prospectus, key investor information document, articles of association and financial reports are available free of charge from the SICAVs’ and management company’s head offices, its representative and distributor in Switzerland, RAM Active Investments S.A., Geneva, and the funds’ representative in the country in which the funds are registered. This marketing document has not been approved by any financial Authority, it is confidential and its total or partial reproduction and distribution are prohibited. Issued in Switzerland by RAM Active Investments S.A. which is authorised and regulated in Switzerland by the Swiss Financial Market Supervisory Authority (FINMA). Issued in the European Union and the EEA by the authorised and regulated Management Company, Mediobanca Management Company SA, 2 Boulevard de la Foire 1528 Luxembourg, Grand Duchy of Luxembourg. The source of the above-mentioned information (except if stated otherwise) is RAM Active Investments SA and the date of reference is the date of this document, end of the previous month.