European Credit: Unlocking Value Despite Spread Compression

The spread compression that has defined credit markets throughout 2024 may lead some investors to hesitate when allocating capital to the asset class. However, RAM AI believes that European credit remains an attractive opportunity, supported by compelling fundamentals and market dynamics.

Yields remain high relative to the last decade

As of January 2025, absolute yields in European credit stood above the 80th percentile of the past decade.

With the European Central Bank’s easing cycle underway, cash rates are expected to decline in the coming months. However, we believe there is still a compelling opportunity to generate attractive income. Steep credit curves should help anchor the longer end of the market and create the potential for capital appreciation as bonds naturally shorten in maturity, with yields drifting lower as they ‘roll down the curve.’

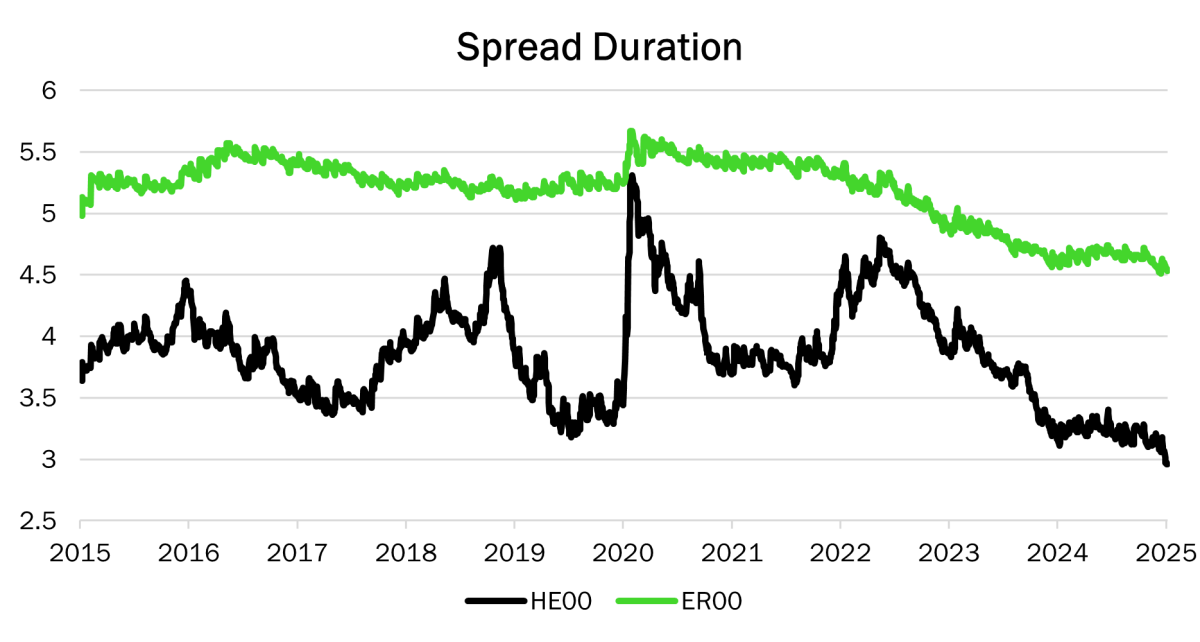

Spreads look attractive on a relative value basis: shorter-duration markets support tighter spreads

The duration of European credit indexes has been declining significantly. Sub-investment grade issuers have opted to retain older bonds issued before the recent cycle of rate increases, capitalising on their lower interest payments, while higher-rated firms have primarily issued bonds with shorter maturities due to their lower financing costs. Simultaneously, the depreciation of longer-dated bonds has reduced their overall weighting in the market. These dynamics have led to European corporate bond markets becoming much shorter in duration than they were at the close of 2021.

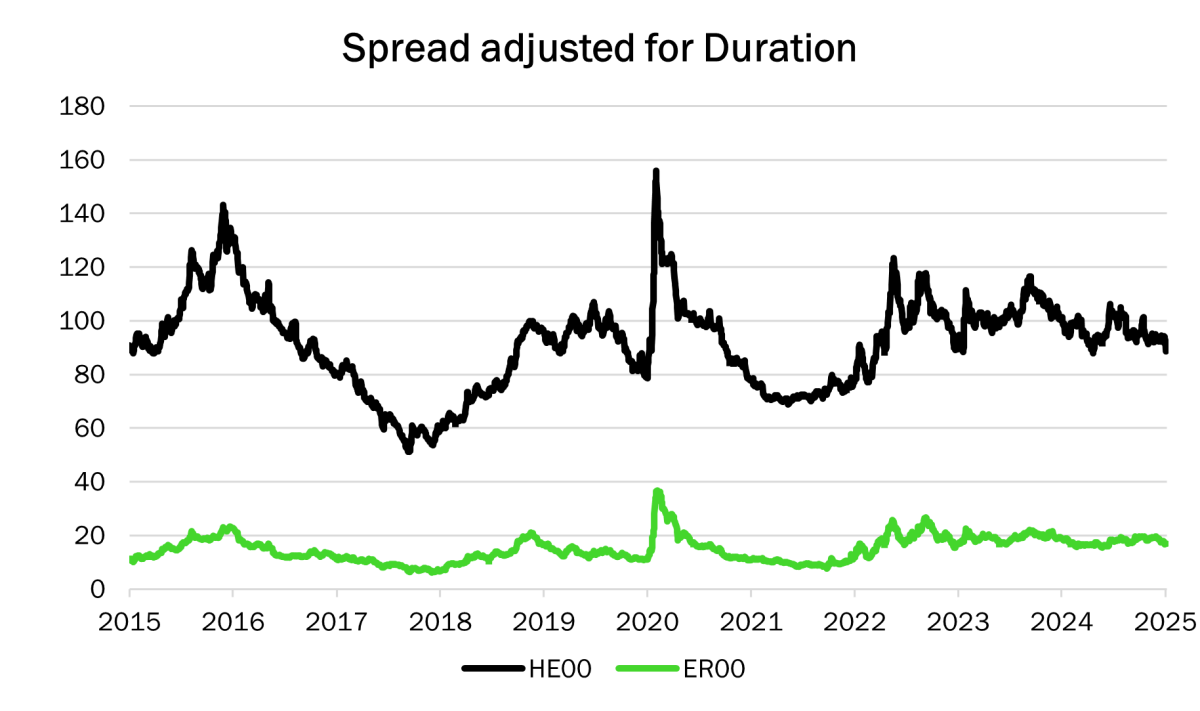

To accurately assess the value in the market, we adjusted spreads for their respective duration. The data indicates that, for each unit of duration, High Yield (HY) bonds currently offer nearly 100 basis points (bps) of spread, while Investment Grade (IG) bonds provide over 20bps. At the end of 2024, spreads in European credit markets were approximately 50% higher per unit of duration compared to their tightest levels in 2018 and 2021. By this metric, European credit spreads appear to have room for further tightening.

By adjusting for duration, we get a better sense of compensation per unit of risk. Investor concerns around spread valuations may be alleviated if we acknowledge that the risks that those spreads reflect are also lower than in the past.

Fundamentals remain solid across the universe

In aggregate, we believe the European credit market benefits from a resilient fundamental backdrop that should help navigate potential market uncertainties with greater stability and confidence.

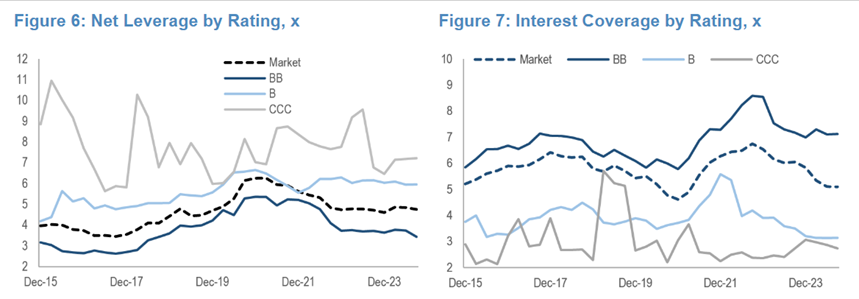

The aggregate interest coverage ratio, which measures a company's ability to cover the interest payments on its outstanding debt, of our credit universe is above the 80th percentile of a period of observation running since 2002 and normalising after a period of very low rates (2015-2021). Similarly, the median net leverage continued to move downward in 2024, trending back towards pre-COVID levels. Interestingly, earnings trends driving the metrics were roughly a 50-50 split on companies seeing EBITDA (Earnings before interest, taxes, depreciation and amortisation) growth vs contraction. Leverage trends by rating continues to flag the dispersion in outcomes between the higher and lower rating bands, with BBs tracking an average 3.6x, back at levels last seen in 2018 while CCCs remain high.

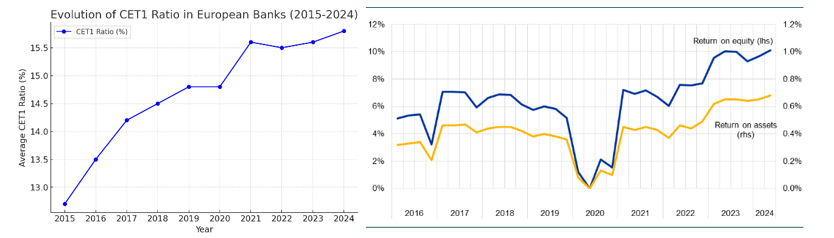

European banks are underpinned by solid fundamentals, supported by strong capital buffers, improved asset quality and resilient profitability. Regulatory reforms over the past decade have strengthened capital positions, with Common Equity Tier 1 (CET1) ratios well above regulatory requirements. Non-performing loan (NPL) ratios have declined significantly, reflecting better risk management and a healthier economic environment. Additionally, higher interest rates have boosted net interest margins, supporting earnings despite a challenging macroeconomic backdrop.

Net leverage and interest coverage are trending down in the European corporate world…

….. while capitalisation and profitability for banks have never been higher

Conclusion

In a scenario where credit demand remains robust and economic or political risks stay under control, our assessment indicates that spreads have still some room for tightening, particularly in the current landscape of exceptionally elevated yields and strong fundamentals.

Image Gallery

Legal Disclaimer

More News & insights

.png)

.png)

.png)