News

9 November 2017

Decrease Your Beta, Diversify Your Sources of Return - Q&A with RAM’s Fixed Income

"Diversify your sources of alpha"

Q&A With Heads of Global Bonds

Why do you think alternative fixed income UCITS deserves increased attention today?

Gilles Pradere: “Supported by very easy monetary policies, major fixed income indices have exhibited strong performance in the last few years, pushing valuations to near record levels. As the global macroeconomic picture is improving, developed market Central Banks are progressively and cautiously, reducing accommodation.

It will definitely be more challenging for a benchmarked portfolio to sustain the same performance with a sudden volatility regime change. Given this backdrop, uncorrelated investment solutions in a UCITS format are a valuable proposition since they don’t fundamentally alter the liquidity profile of a fixed income portfolio.”

“Flexibility has clearly become a necessity to navigate today’s markets”

What is the main challenge facing fixed income investors in the current environment?

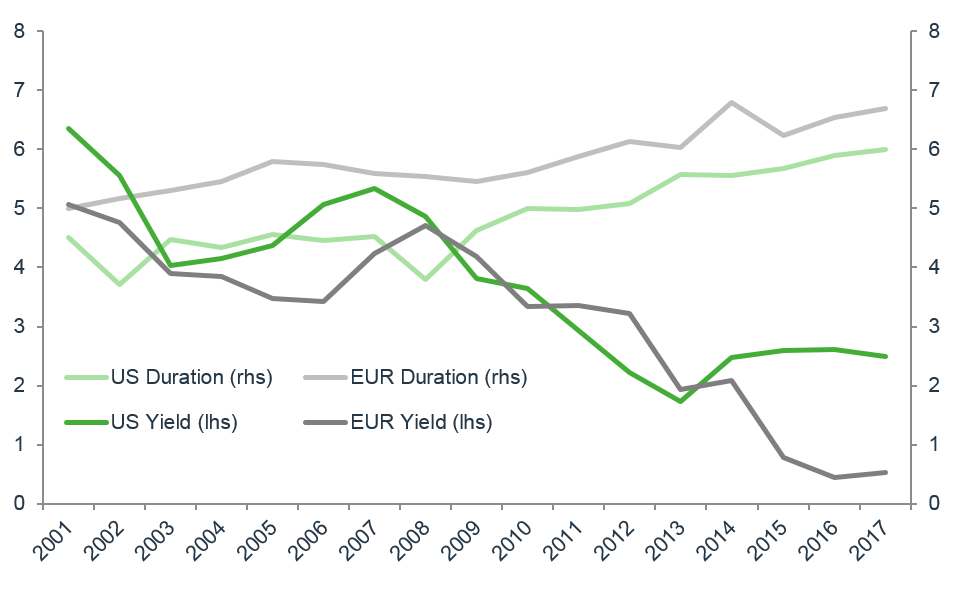

Gilles Pradere: "Government and corporate bond yields expose investors to potential large losses in a rates normalisation process. To illustrate this point, the Barclays Global Aggregate Index, which is a flagship measure of global Investment Grade debt, has a duration of more than six years, for a running yield of less than 2% (see graph overleaf). In other words, a 1% adverse interest rate move would generate a loss of 6%, which is the equivalent of three full years of coupon.

Traditionally, one way to circumvent these low government bonds yields was to invest in corporate bonds. But with a large part of the Investment Grade bond universe displaying low yields, the temptation is high to move down the credit ladder and invest in High Yield bonds. This behaviour undermines the diversifying objective of a fixed income allocation due to the strong correlation between High Yield and equities. Instead of switching duration risk for credit risk, we believe it is possible to keep a high average credit quality portfolio and deliver an asymmetrical risk/return profile.".

What would be a sensible investment approach in this environment?

Gilles Pradere: "Fexibility has clearly become a necessity to navigate today’s markets. In other words, a traditional bond portfolio, which is actively managed in terms of duration and credit risks, could be complemented with sources of performance screened in credit, rates and forex markets. By using available liquid instruments in an appropriate and disciplined way, these additional performance engines - also called non-traditional strategies - offer uncorrelated return opportunities and can immunise partially or fully some portfolio risks.*

*(Please refer to the latest Fund’s Prospectus to obtain further information on risks associated with investments).

A More Complex Fixed Income Environment

Past performance is not a reliable indicator of future results. Please refer to the disclaimer at the end of this document.

How do you articulate a flexible investment mandate for your Strategy?

Gilles Pradere: The aim of our investment philosophy is medium term capital appreciation with efficient downside risk management. In other words, we want to be adequately compensated for the risks we take. We rely on four major pillars to implement our approach

We are benchmark-agnostic. An unconstrained and flexible approach enables us to be tactical and chase opportunities where they arise.

- We keep a high level of diversification in terms of regions, strategies, sectors and positions. Our goal is to capitalise on a large number of strategies and minimise idiosyncratic risk.

- Maintain a strong credit quality in the portfolio. This represents a key part of our value proposition, as our main focus is on Investment Grade issuers.

- Pursue a disciplined approach to ensure sustainability. Thus, every position in the portfolio follows a consistent and repeatable investment process.

We believe a strict application of our principles will deliver an asymmetric risk/return profile to investors.

What are the exact additional sources of return for your Strategy?

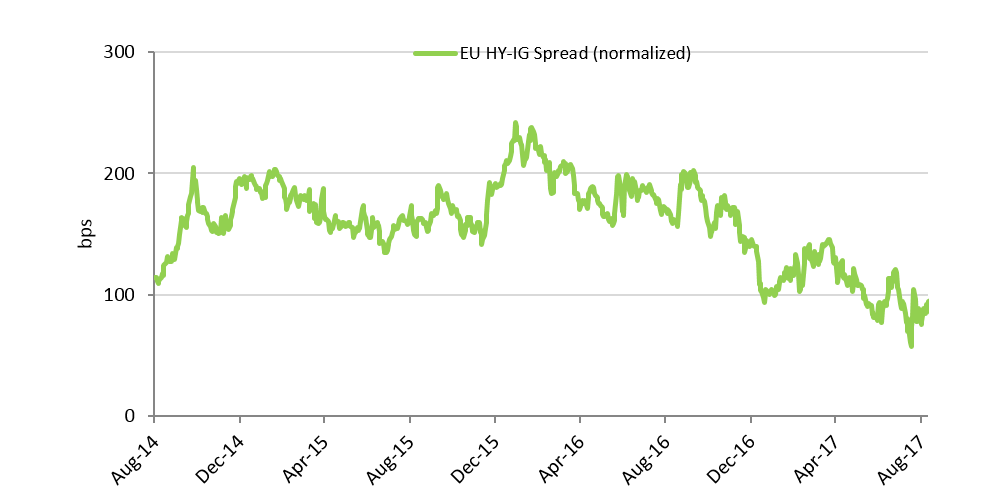

Clément Perrette: "When we screen for non-traditional trades, our aim is to seize rates relative value opportunities in rates and credit, as well as filter value in local currency bonds and FX markets. By doing so, we are mainly looking for asymmetrical investment profiles. For instance, European High Yield appears to be richly priced against Investment Grade in an historical context (see graph below). It is possible to implement a carry-neutral trade with limited downside that would be of benefit in the event of a HY credit risk repricing.

Another source of diversification consists of our FX allocation, which is an important element to effectively accessing local currency bonds, presenting real yield opportunities. Combined with the attractive medium-term valuation of the currency, those positive real yields would act as a protection buffer. It is also worth noting that individual exposures are kept moderate, in line with our diversified approach."

EU HY-IG Spread (Normalised)

Past performance is not a reliable indicator of future results. Please refer to the disclaimer at the end of this document.

How would performance between traditional and non-correlated strategies evolve through time?

Gilles Pradere: "The current environment, characterised by low volatility, is conducive to traditional strategies. As a result, we have been able to extract most of the value from this bucket. That said, our non-traditional strategies also had a significant positive performance contribution, despite a less favourable environment. If volatility returns to fixed income markets, we expect more opportunities to appear in nontraditional strategies.

“Supported by very easy monetary policies, major fixed income indices have exhibited stron“Flexibility has clearly become a necessity to navigate today’s markets”

Indeed, both traditional and non-traditional strategies should contribute positively over a two-to-three year investment horizon. With different performance engines taking the lead over time, we aim to protect on the downside and ensure capital appreciation."

Finally, for which type of major risks is the Strategy prepared?

Gilles Pradere: "There are several potential risks that could arise in the medium term. To start with, the policy normalisation process initiated by the Fed might be followed by the BoE and ECB. This slow dismantlement of post Global Financial Crisis policies will certainly not be an uneventful process. As a result, we have been running the Strategy with moderate duration. On the geopolitical side, tensions could readily resurface.

Even if those events are unpredictable by nature, some of our uncorrelated strategies are designed to benefit from a higher volatility environment.

China remains one of the major question marks due to the high level of corporate debt. This is why, with China, we focus on sovereign and quasi-sovereign debt. In conclusion, we believe our approach combining flexibility, diversification and high credit quality could be successful over the coming quarters."

Past performance is not a reliable indicator of future results. Please refer to the disclaimer at the end of this document.

Important Information:

This document has been drawn up for information purposes only. It is neither an offer nor an invitation to buy or sell the investment products mentioned herein and may not be interpreted as an investment advisory service. It is not intended to be distributed, published or used in a jurisdiction where such distribution, publication or use is prohibited, and is not intended for any person or entity to whom or to which it would be illegal to address such a document. In particular, the products mentioned herein are not offered for sale in the United States or its territories and possessions, nor to any US person (citizens or residents of the United States of America). Important warning to clients in some countries, please note that the Sub-fund: RAM (Lux) TACTICAL FUNDS-Global Total Return Fund is not currently registered for distribution in Sweden, Denmark, Finland and Norway. RAM (Lux) SYSTEMATIC FUNDS- Long/Short Global Equities Fund is not currently registered for distribution in Denmark, Portugal and Singapore. The opinions expressed herein do not take into account each customer’s individual situation, objectives or needs. Customers should form their own opinion about any security or financial product mentioned in this document. Prior to any transaction, customers should check whether it is suited to their personal situation and analyse the specific risks incurred, especially financial, legal and tax risks, and consult professional advisers if necessary. The information and analyses contained in this document are based on sources deemed to be reliable. However, RAM cannot guarantee that said information and analyses are up-to-date, accurate or exhaustive, and accepts no liability for any loss or damage that may result from their use. All information and assessments are subject to change without notice. Investors are advised to base their decision whether or not to invest in fund shares on the most recent financial reports, key investor information document (KIID) and prospectus which contain further information on the products concerned. The value of shares and income thereon may rise or fall and is in no way guaranteed. The price of the financial products mentioned in this document may fluctuate and drop both suddenly and sharply, and it is even possible that all money invested may be lost. Changes in exchange rates may cause the NAV per share in the investor's base currency to fluctuate. If requested, RAM Active Investments S.A. will provide customers with more detailed information on the risks attached to specific investments. Exchange rate variations may also cause the value of an investment to rise or fall. Whether real or simulated, past performance is not necessarily a reliable guide to future performance. The prospectus, KIID, articles of association and financial reports are available free of charge on www.ram-ai.com, from the SICAV’s and Management Company’s registered offices, its representative and distributor in Switzerland, RAM Active Investments S.A., Geneva, and the SICAV’s representative in the country in which the SICAVs are registered. This marketing document has not been approved by any financial Authority, it is confidential and addressed solely to its intended recipient; its reproduction and distribution are prohibited. RAM Active Investments S.A. is authorised and regulated in Switzerland by the Swiss Financial Market Supervisory Authority (FINMA). Issued in the UK to professional investors only by RAM Active Investments (UK) Limited, 35 Berkeley Square, London W1J5BF, incorporated in England and Wales, No 9338325. Issued in the Continental Europe by the Management Company RAM Active Investments (Luxembourg) S.A., 51 av. John F. Kennedy L-1855 Luxembourg, Grand Duchy of Luxembourg.