Commentaries

12 October 2020

September 2020 - Healthy stock picking benefits diversified equity strategies - Systematic Fund Manager's Comments

The global equity market stalled in September after having posted five months of consecutive positive return. Uncertainties linked to further fiscal stimulus and the presidential election in the US, the acceleration in new Covid-19 infection cases, and discussions related to EU/UK trade deal fuelled a risk assessment of portfolios by investors.

Besides the Technology sector retreat, which was widely expected to happen at some point considering its exponential rise, it was more interesting to observe that stocks with weak fundamentals largely underperformed the market. Among the reasons why stocks exhibiting pre-existing fragility lagged the market, the increase in Covid-19 infection cases was certainly the catalyst. However, when we analyse the dynamic of these names through the lens of the below metrics, the market action was more than justified:

- Free Cash Flow

- Debt/Equity

- Earnings Estimates

- Book Value

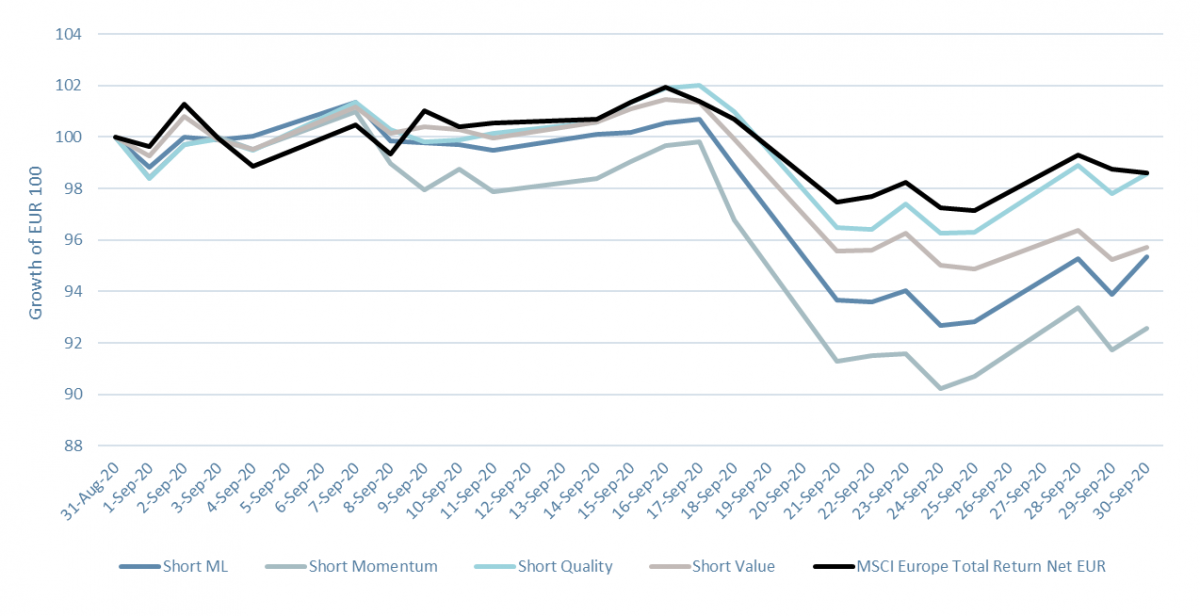

Our systematic equity strategies focused on Europe were able to capture strong alpha in both long and short books. The below chart highlights the underperformance of stocks held in the short strategies of RAM Long/Short European Equities versus the market.

Short Selections in RAM Long/Short European Equities vs MSCI Europe TRN

Source: Bloomberg, RAM AI, as of 30.09.2020

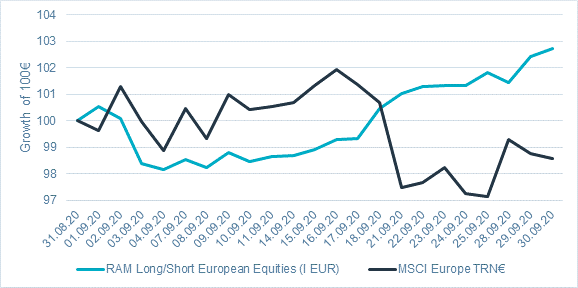

With long selections also being able to generate positive alpha, RAM Long/Short European Equities (I EUR) closed the month comfortably up, evidencing its uncorrelated virtue within a portfolio context.

RAM Long/Short European Equities (I EUR) vs MSCI Europe TR

Source: Bloomberg, RAM AI, as of 30.09.2020

The high dispersion in the market continues to be a source of opportunities for diversified equity solutions from a strategy and market capitalisation perspective. The September move represents a harbinger of what could happen if stock picking takes a center stage over an extended period.

Finally, we have filtered the European equity market to analyse companies having over EUR 150 million market capitalisation with low credit metrics (Net Debt/Equity >100%, Cash Coverage <1, Liability/Asset Ratio > 60%). There are 226 companies, with most of them having their bonds rated High Yield. The average default probability (as calculated by Bloomberg) is at 1.0% for these companies, which seems to be rather optimistic given the weak fundamentals for these companies and the political/macro uncertainties.

Direct access per fund to our latest Fund Manager's Comments:

Legal Disclaimer

This document has been drawn up for information purposes only. It is neither an offer nor an invitation to buy or sell the investment products mentioned herein and may not be interpreted as an investment advisory service. It is not intended to be distributed, published or used in a jurisdiction where such distribution, publication or use is prohibited, and is not intended for any person or entity to whom or to which it would be illegal to address such a document. In particular, the products mentioned herein are not offered for sale in the United States or its territories and possessions, nor to any US person (citizens or residents of the United States of America). The opinions expressed herein do not take into account each customer’s individual situation, objectives or needs. Customers should form their own opinion about any security or financial instrument mentioned in this document. Prior to any transaction, customers should check whether it is suited to their personal situation and analyse the specific risks incurred, especially financial, legal and tax risks, and consult professional advisers if necessary. The information and analyses contained in this document are based on sources deemed to be reliable. However, RAM AI Group cannot guarantee that said information and analyses are up-to-date, accurate or exhaustive, and accepts no liability for any loss or damage that may result from their use. All information and assessments are subject to change without notice. Investors are advised to base their decision whether or not to invest in fund units on the most recent reports and prospectuses. These contain further information on the products concerned. The value of units and income thereon may rise or fall and is in no way guaranteed. The price of the financial products mentioned in this document may fluctuate and drop both suddenly and sharply, and it is even possible that all money invested may be lost. If requested, RAM AI Group will provide customers with more detailed information on the risks attached to specific investments. Exchange rate variations may also cause the value of an investment to rise or fall. Whether real or simulated, past performance is not necessarily a reliable guide to future performance. The prospectus, key investor information document, articles of association and financial reports are available free of charge from the SICAVs’ and management company’s head offices, its representative and distributor in Switzerland, RAM Active Investments S.A., Geneva, and the funds’ representative in the country in which the funds are registered. This marketing document has not been approved by any financial Authority, it is confidential and its total or partial reproduction and distribution are prohibited. Issued in Switzerland by RAM Active Investments S.A. which is authorised and regulated in Switzerland by the Swiss Financial Market Supervisory Authority (FINMA). Issued in the European Union and the EEA by the Management Company RAM Active Investments (Europe) S.A., 51 av. John F. Kennedy L-1855 Luxembourg, Grand Duchy of Luxembourg. The reference to RAM AI Group includes both entities, RAM Active Investments S.A. and RAM Active Investments (Europe) S.A.